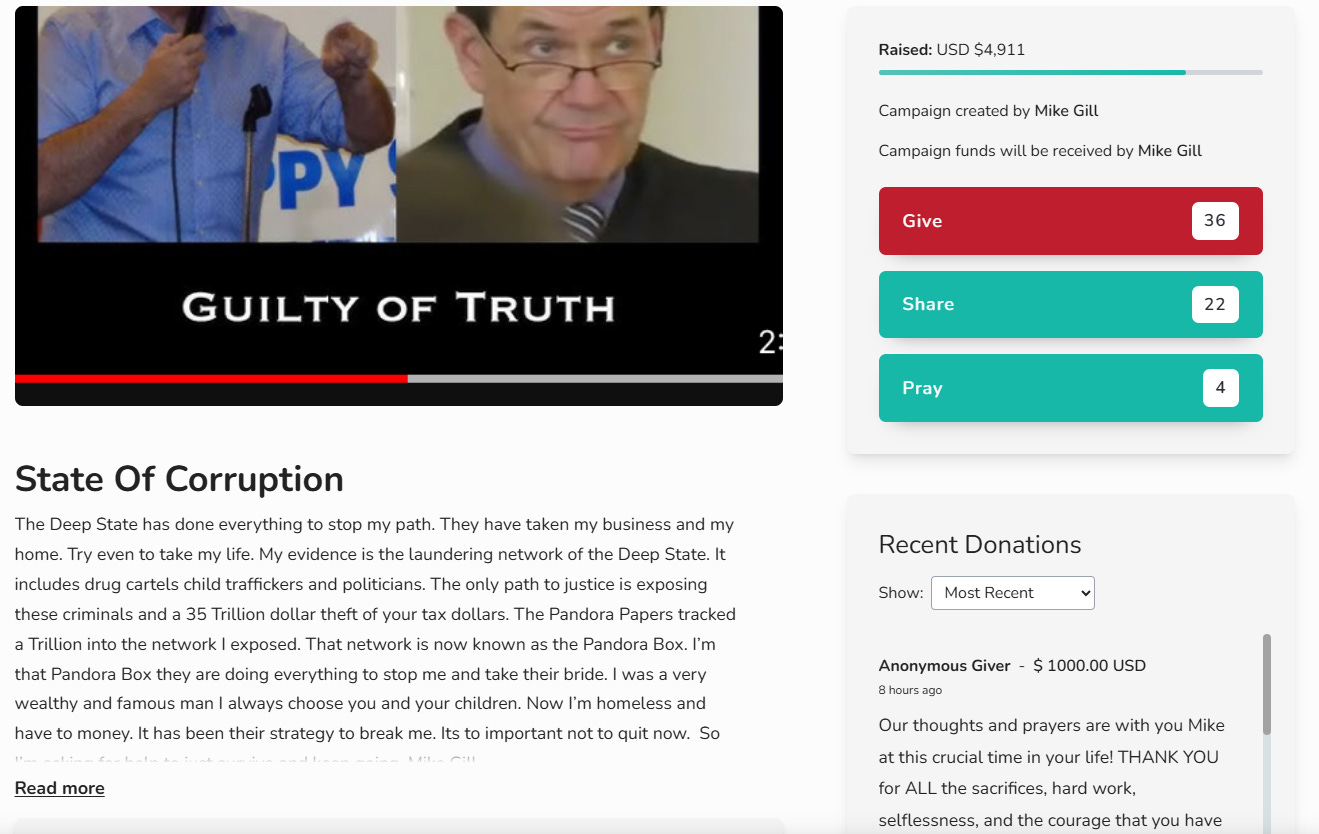

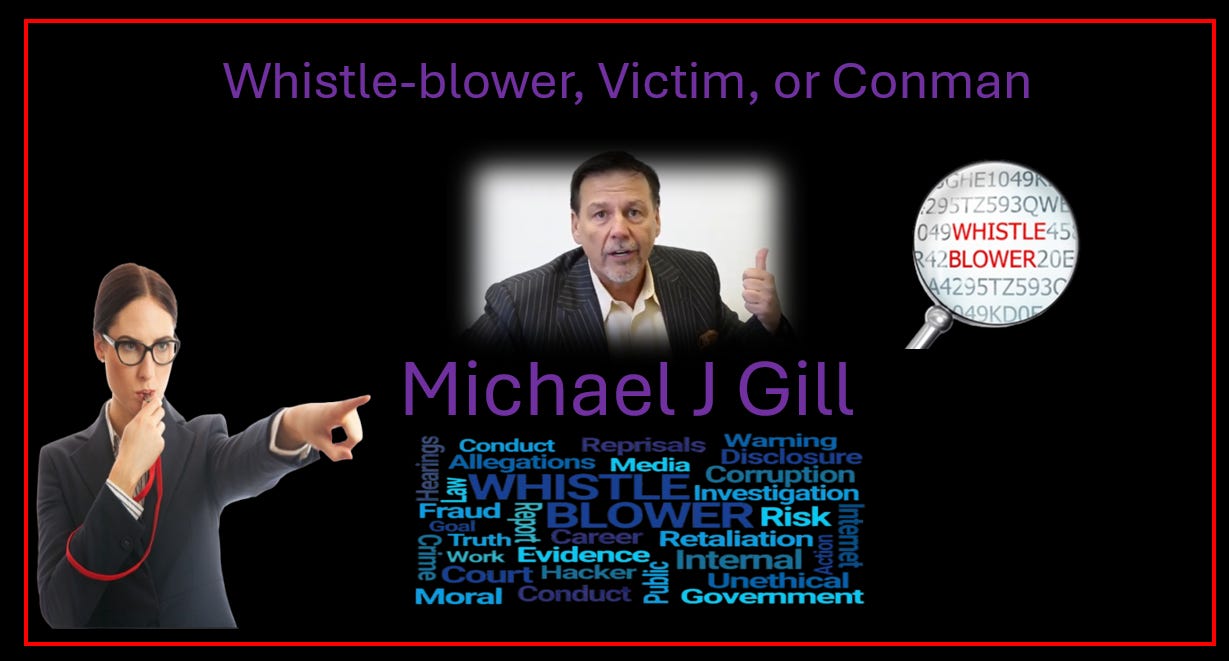

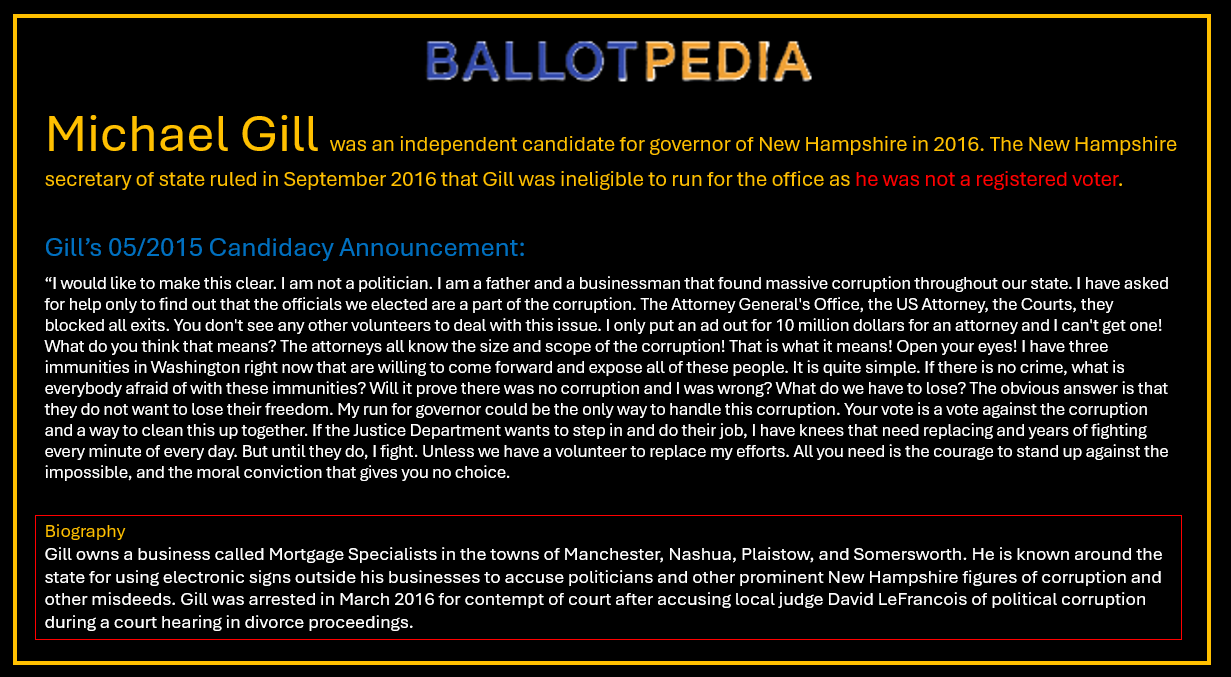

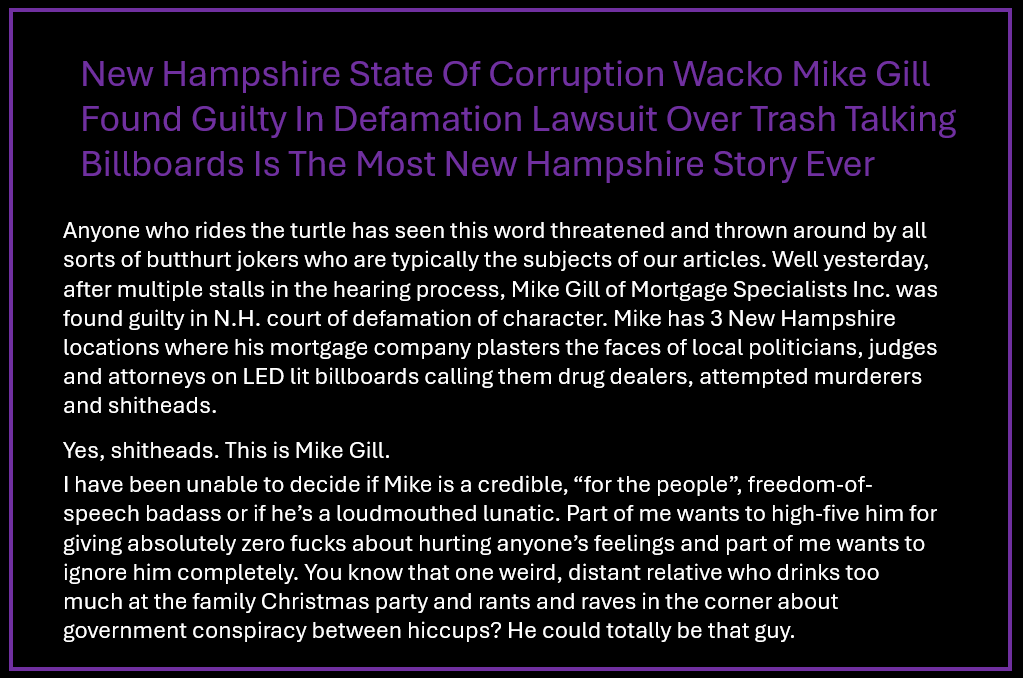

Mike Gill

Whistleblower, Victim, or Conman

I first really heard Mike Gill and his “Pandora’s Box” claims on the Michelle Moore Show early this year. A few months later, Mike was in Arizona and began discussing our politics. His association with John Thaler, Liz Harris and Shelby Bush put Mike Gill firmly on my radar. Did I mention, I reside in Arizona, I am autistic, female and post-menopausal? In other words, Mike set off my bullshit meter and the bloviating bully is just too easy a target to pass up.

Spoiler Alert, the guy’s media droppings sure mirror the attributes of a sociopath. As you will see he is chronically mired in controversy, always accused, but never at fault. He sues for defamation at the drop of a hat, yet he is quick to throw out defamatory statements about anyone who questions him. Without further ado, lets dive into Mike Gill’s story, from his rise in the mid 90’s through the present.

In the Beginning…

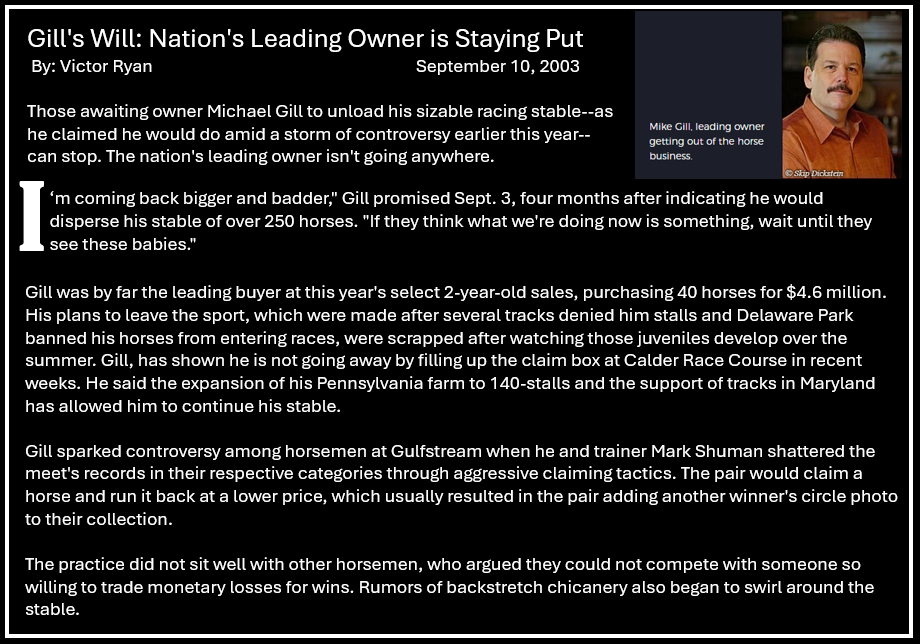

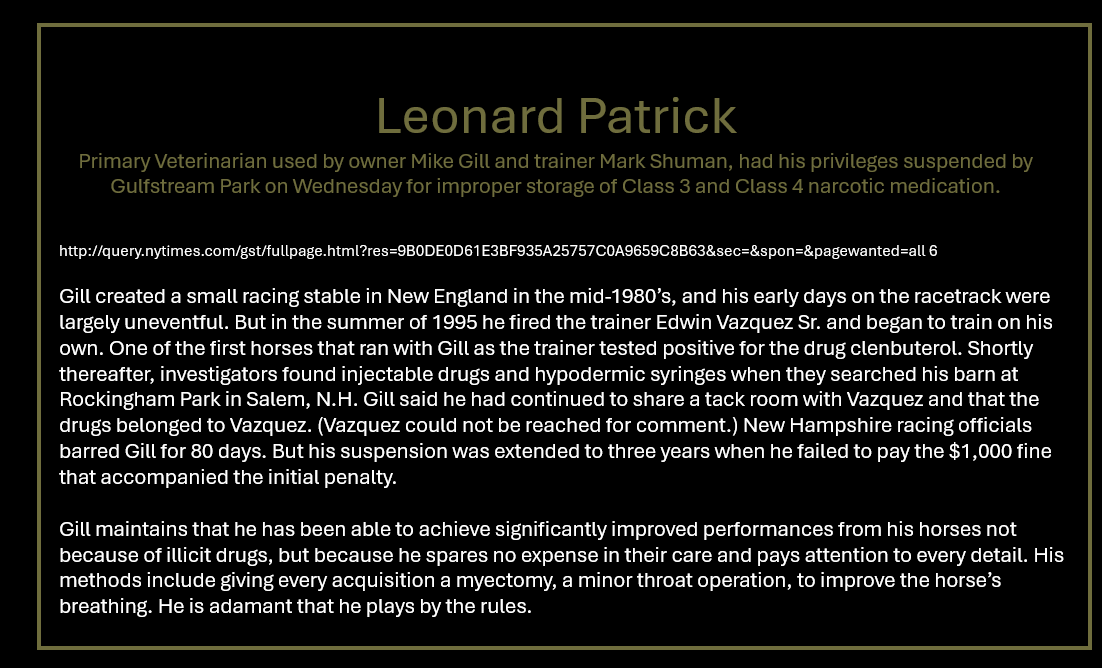

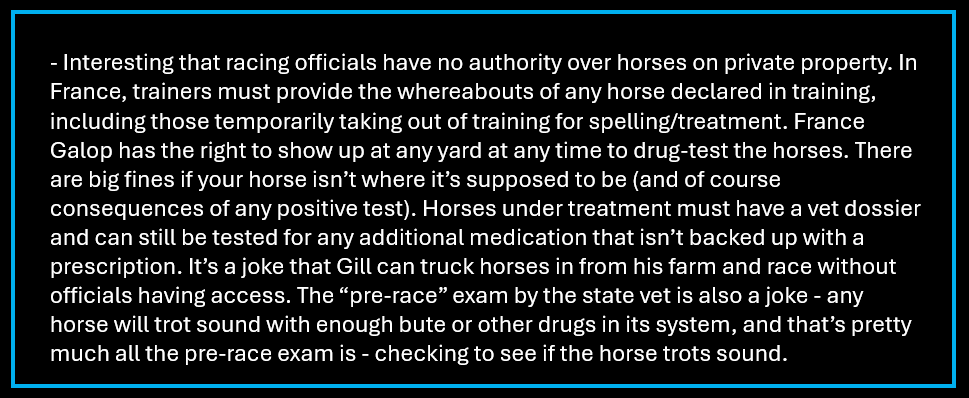

In the mid 80’s Gill had a small racing stable in New England. Mike’s presence in racing for the first decade was largely unremarkable. That changed the summer of 1995, when the first horse he ran as the trainer and owner tested positive for the drug clenbuterol. An investigation and search of his Rockingham Park barn provided the evidence of doping. The search yielded injectable drugs and hypodermic syringes.

Gill claimed they belonged to Edwin Vazquez, Sr, whom he fired yet still shared a tack room. Interestingly, Mike did not have dirty tests when Vasquez was the trainer, and Vasquez’ horse, post firing, was not found dirty, yet they belong to Vasquez. I am not buying it, but then neither did New Hampshire racing officials. They barred Gill for 80 days and fined him $1,000.00. He refused to pay and was subsequently barred until he paid the fine a little over 3 years later in 1999, so he could once again race.

I am gonna party like its 1999

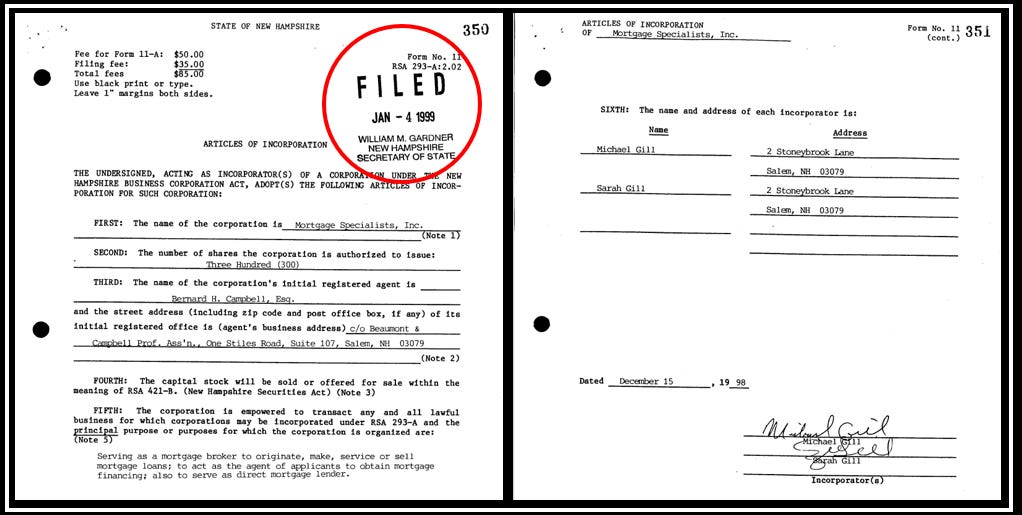

In 1998, Gill and his wife open the Mortgage Specialists. Subprime loans were new, and they paid well. At that time, you could put a marginal borrower in a house for little down, deferred student loans on an adjustable rate and make 4 points up front and 4 points on the backside. So, in other words, you could “qualify” someone that couldn’t really afford. Never mind you just created a future foreclosure because you just made 8% on that loan.

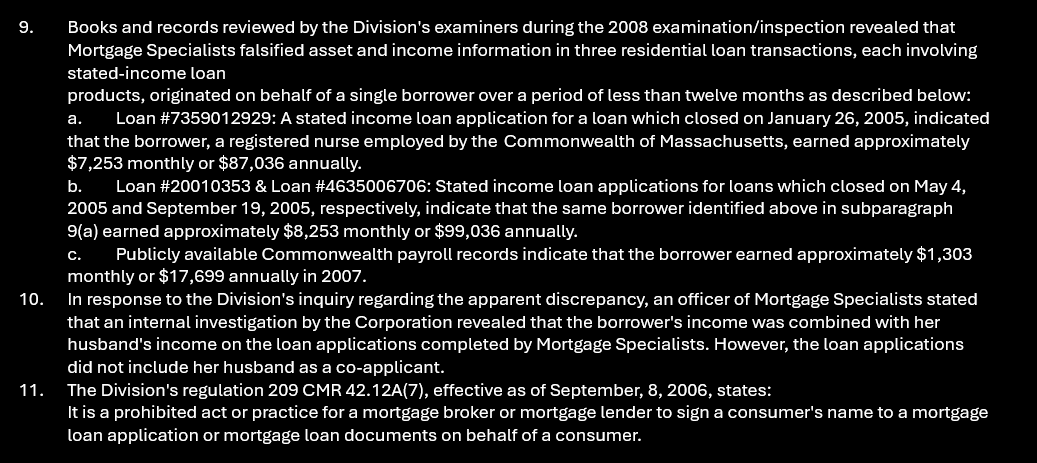

80% of subprime loans were adjustable-rate mortgages, and between 1995 and 2001 thy jumped from 65-173 billion a year. Congress passing the Gramm–Leach–Bliley Act, otherwise known as the Financial Services Modernization Act of 1999, which repealed the Glass–Steagall Act less was like pouring gas on a fire. The repeal of Glass–Steagall removed the restrictions that had effectively separated the activities of commercial banks and investment banks and securities firms. This paved the way for commercial banks to roll out the mortgage-backed security.

Because we were also coming off the dot com bubble, investors were looking for more tangible investments so of course as we all know they jumped in with both feet. It seems Mike was able to capitalize on the subprime market as the New York Times reports in their April 16, 2003, article entitled “Horse Racing leaves a bitter taste in owner’s mouth, that when Gill returned in 1999 “with deep pockets, having hit it big in the mortgage business.”

Just 2 years later on May 15, 2002, the New Hampshire Banking Department denied Mortgage Specialists' application for license renewal ''on the grounds that the applicant's financial resources, experience, personnel and record of past or proposed conduct do not warrant the public's confidence and the issuance of a license”.

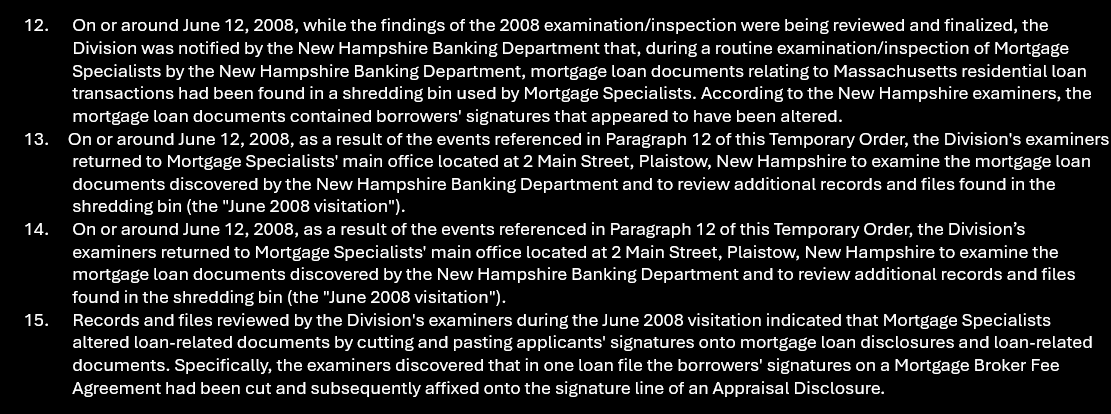

He appealed promising to procure the services of a compliance officer and to issue some borrower refunds, and the Banking Department approved Gill's license renewal. At the time, he said it was just a minor issue that involved his opening a branch office before the license was in order. The Banking Department declined to comment.

The house that “I” Built

Mike is constantly saying he has been in this fight for 18 years. So far, the moment Mike begins to inject, err I mean train his own horses, the horse tests dirty, he blames his former trainer. A trainer who was running another horse and his horse did not test dirty, Mike’s horses for the decade he trained them never came up dirty. Things that make you call bullshit.

He returned in 1999 to horse racing “flush with cash” after hitting it big in the mortgage business, a business he just entered the year before. Within the first three years, he was denied a renewal of his license and had to agree to remedy his lack of compliance. Things that make you go hmm.

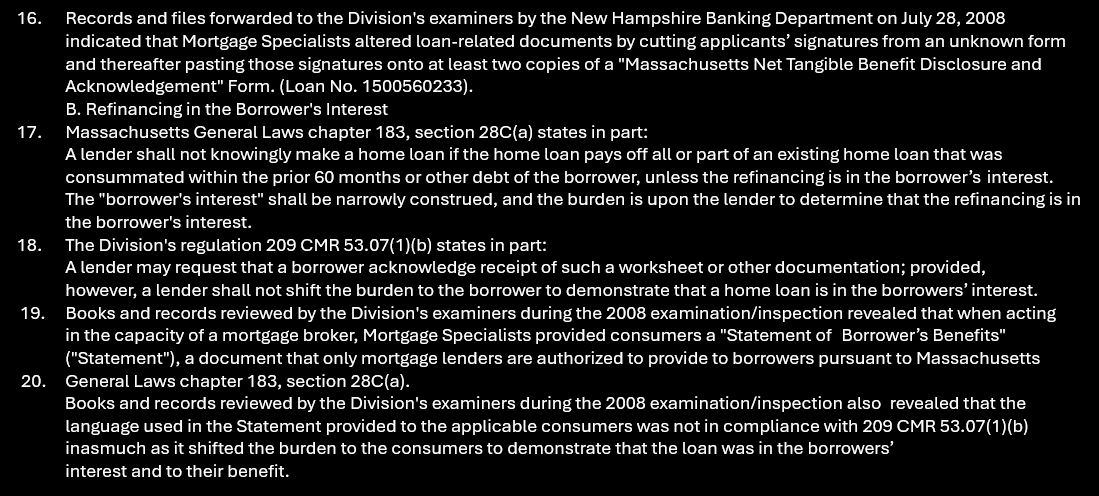

More Headlines

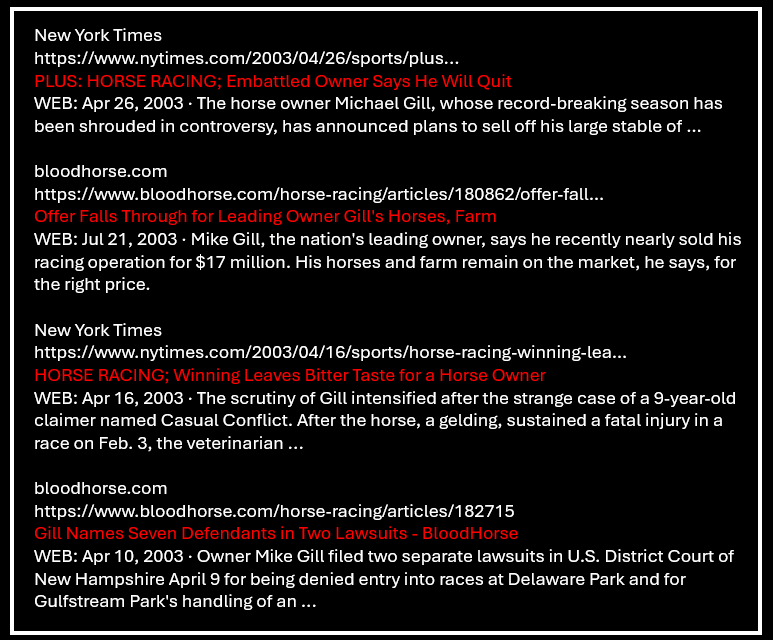

Let the Suits Begin - A Season of Lawfare

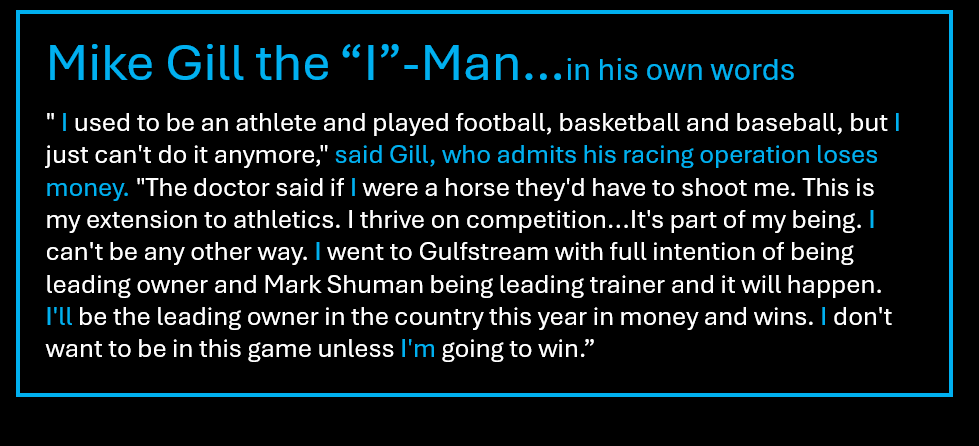

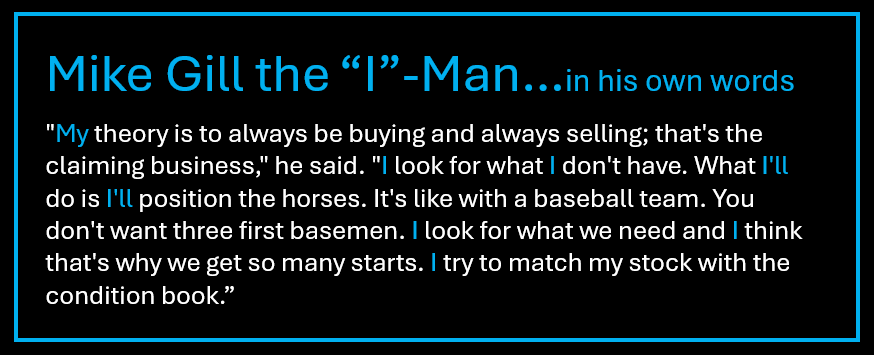

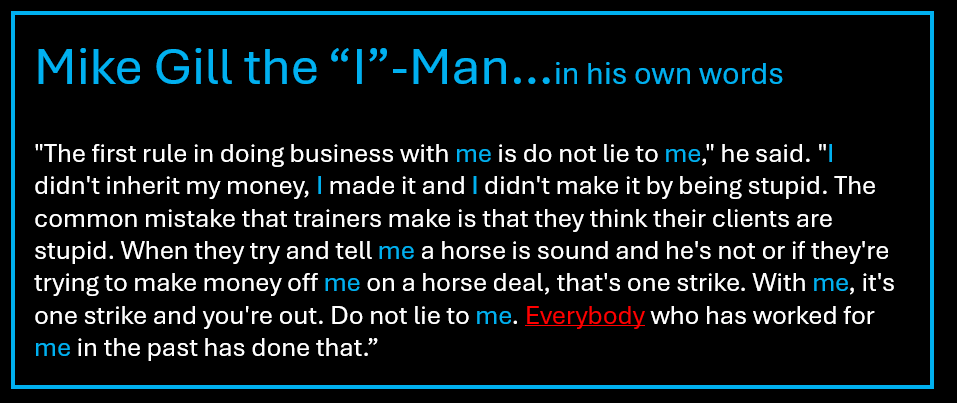

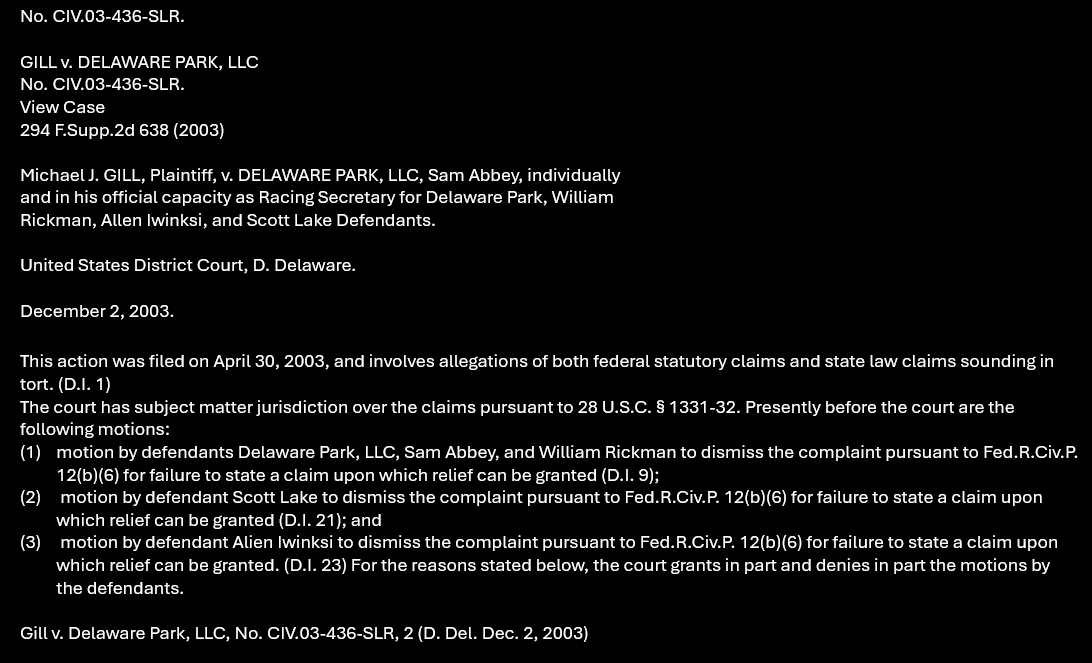

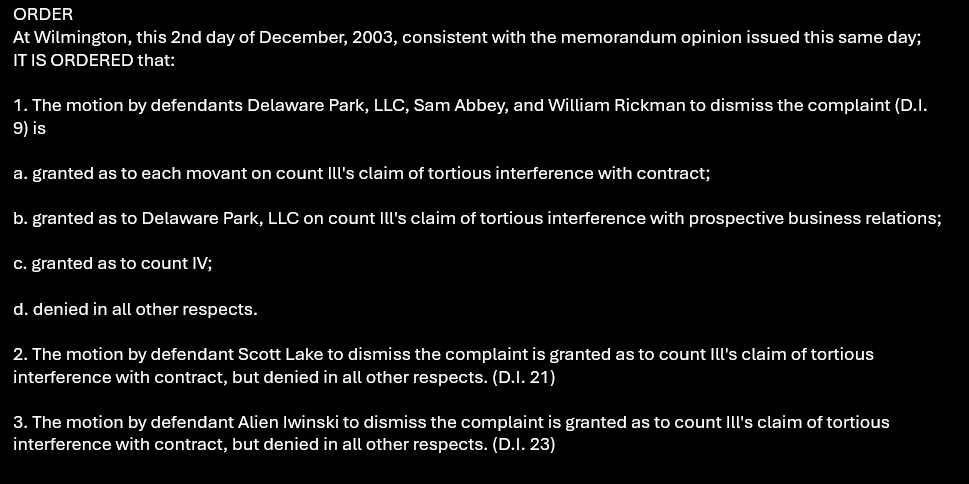

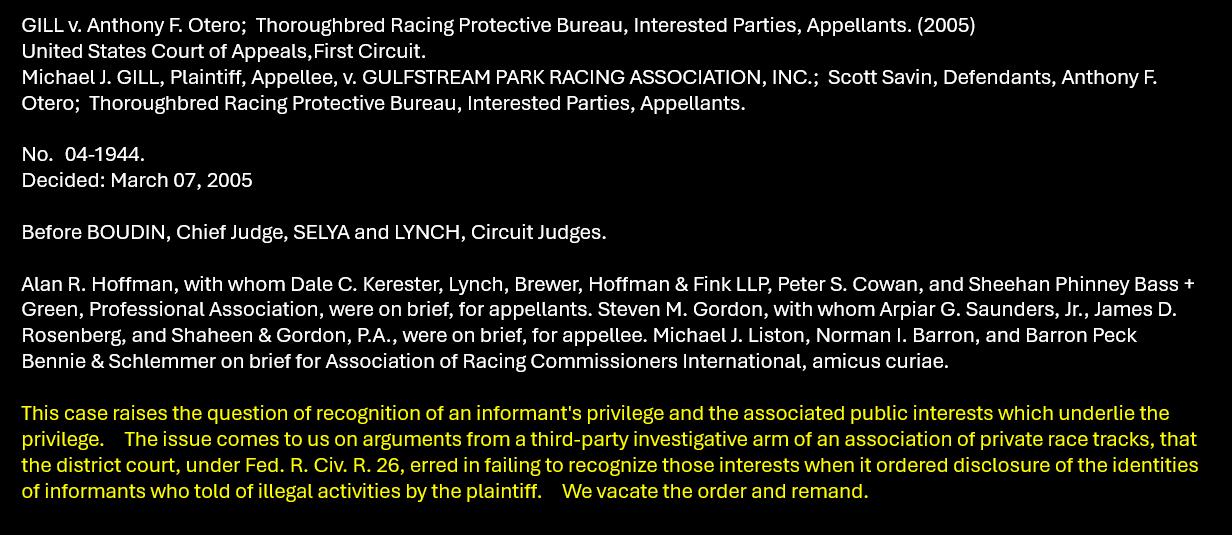

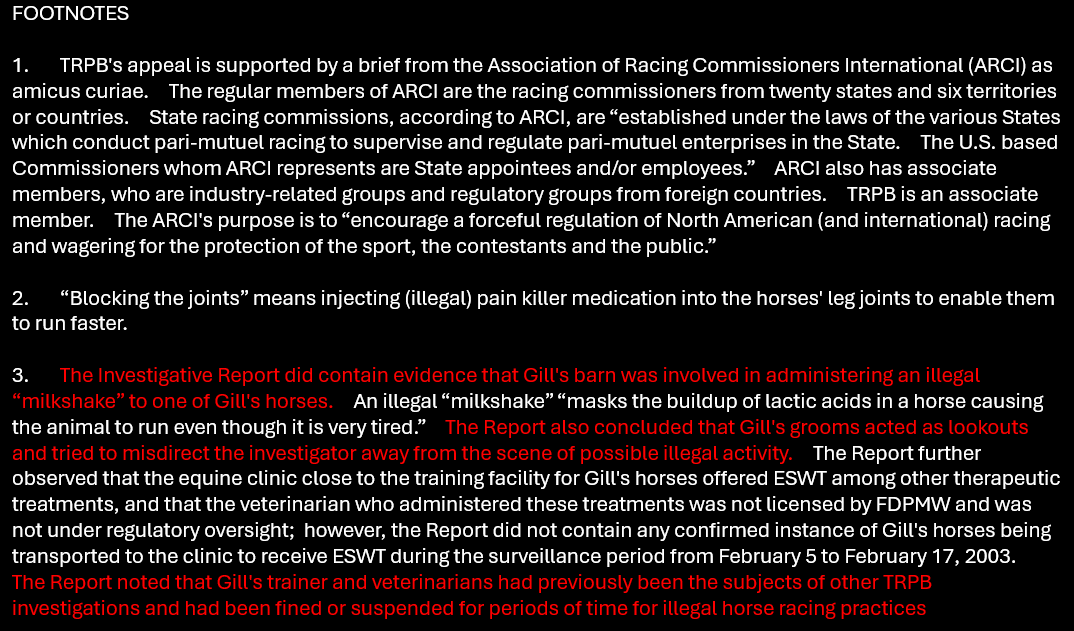

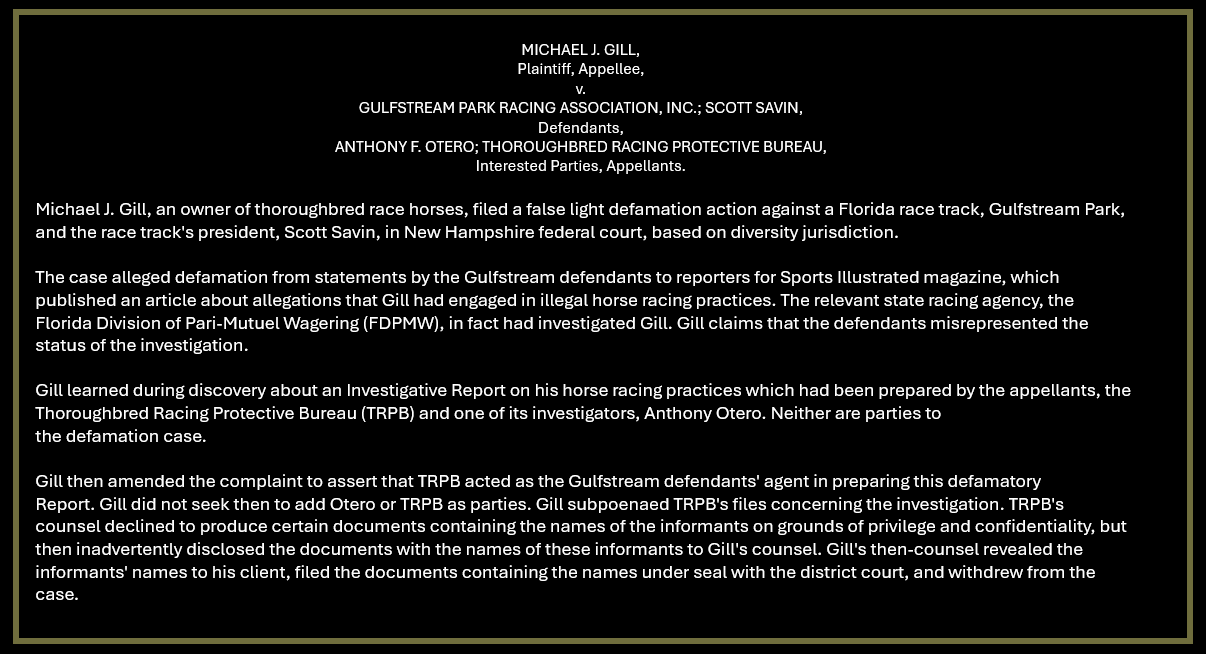

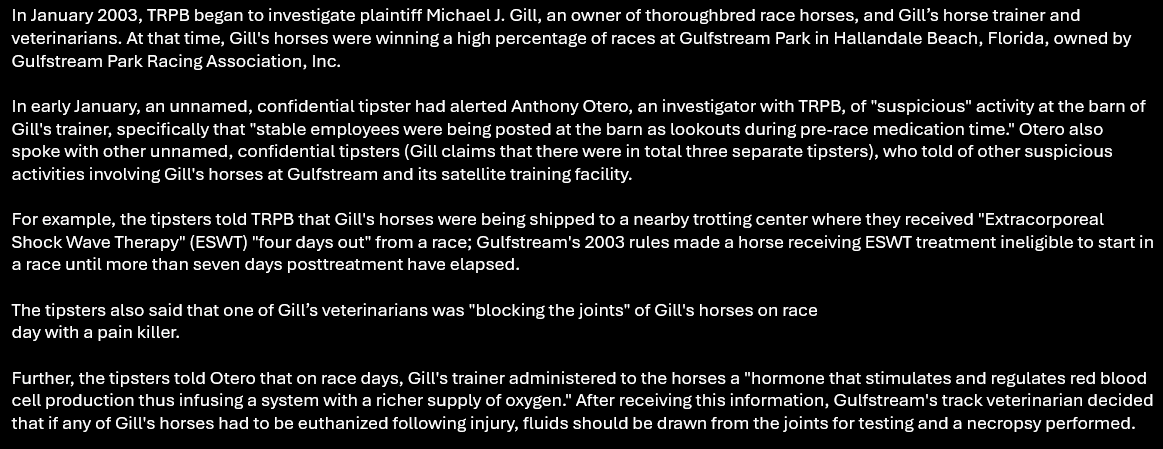

Its 2003 and just a few short years since he re-entered horse racing after leaving on a doping suspension and again he is found doping, so Mike responded by filing defamation and tortious interference lawsuits against Delaware and Gulfstream parks. Mike lost on defamation in both cases and did not regain track stall privileges. Infact, the Otero Gulfstream case enshrined in court documentation that he in fact was doping at least one horse.

In Gulfstream, Mike’s claims fared no better, and it evidenced his doping activity.

Case Footnotes show Gill was “milkshaking”. Again, Gill lost on the defamation.

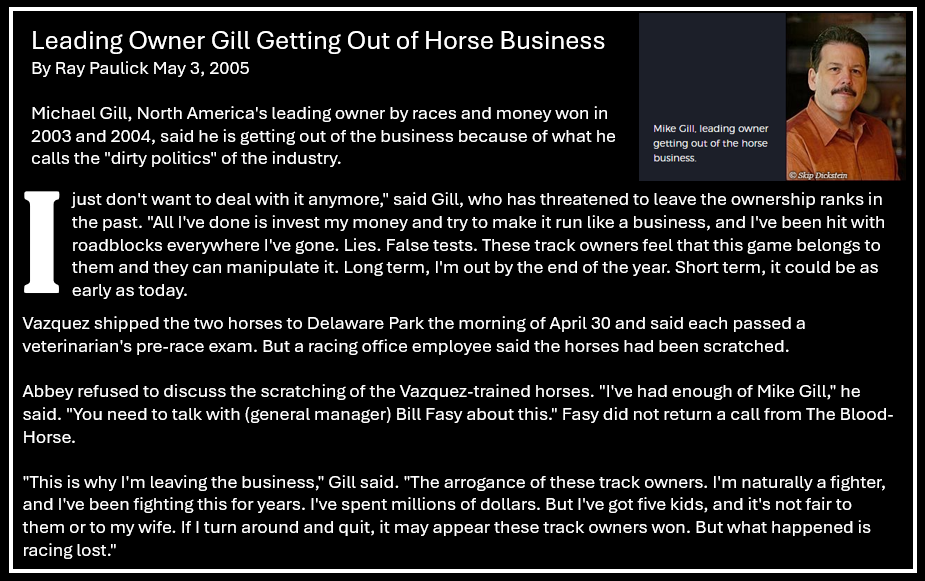

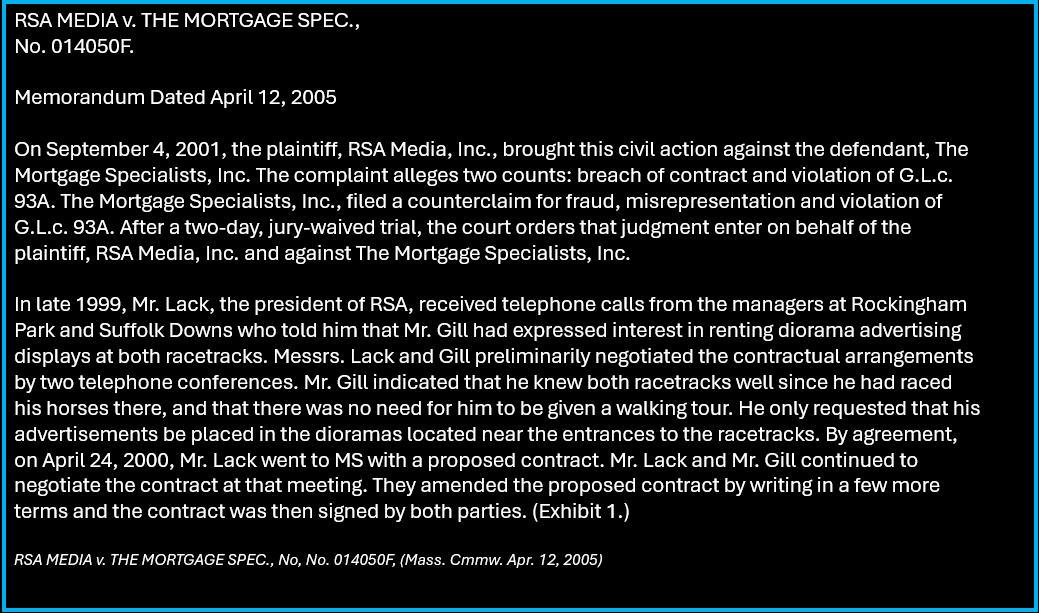

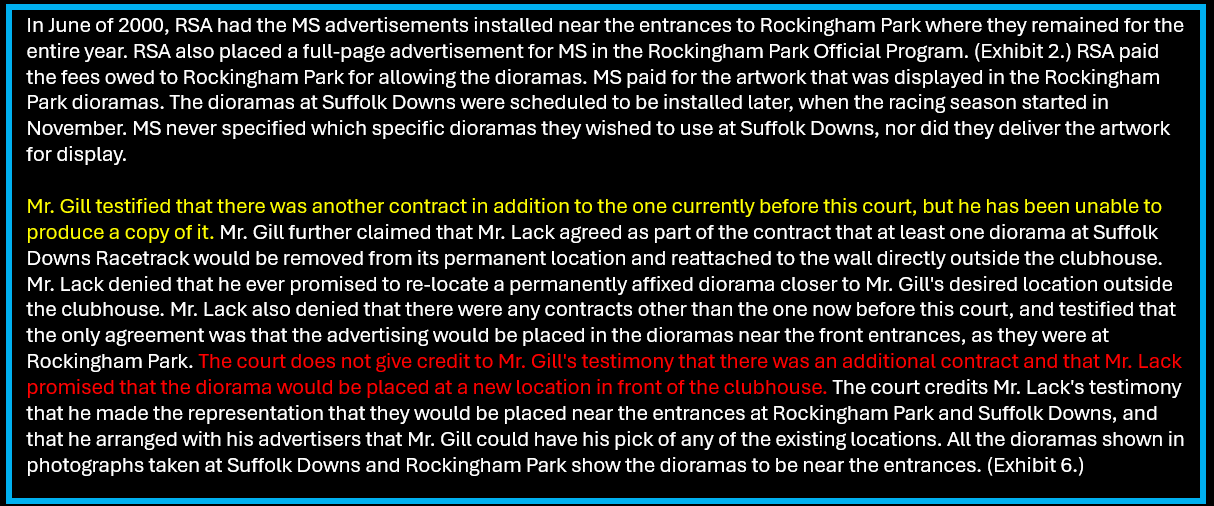

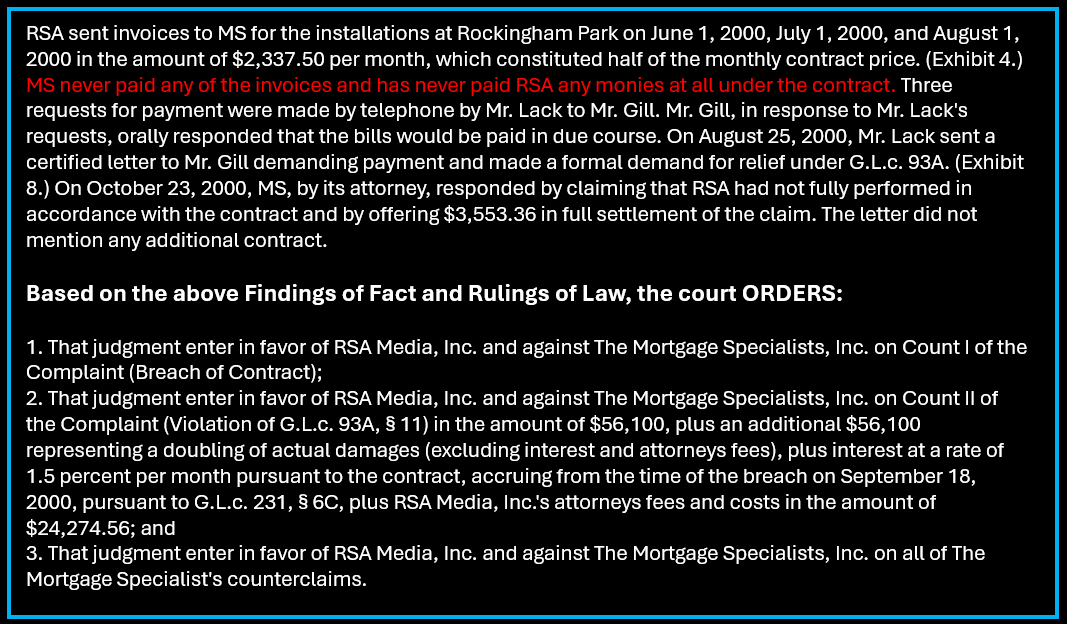

Is the stable that “I” built crumbling after his losses in all his cases. Hmm, he also has a case brought against him, by RSA Media, it’s just below the article of Guilty Gill levying more allegations dirty politics of horse racing and of course he is the target, because he is so much smarter and better than anyone else.

In this case brought against Mike in 2005, we find Mike not paying his bills. This is a reoccurring issue with Mike. I find the irony just too much; this is Mike’s first foray with billboards and ends up in a lawsuit and judgement against Mike.

Mike’s Manifesto

Well, its 2006 and that brings us to Mike’s 44 Page Manifesto he published on Scribd. This was not published in 2006, but his “recollections” begin there. Mike begins, in 2006, where we find Mike having marital issues, IRS issues, and it seems all the attorneys in NH are conspiring against him. We are going to follow along and see what we can verify.

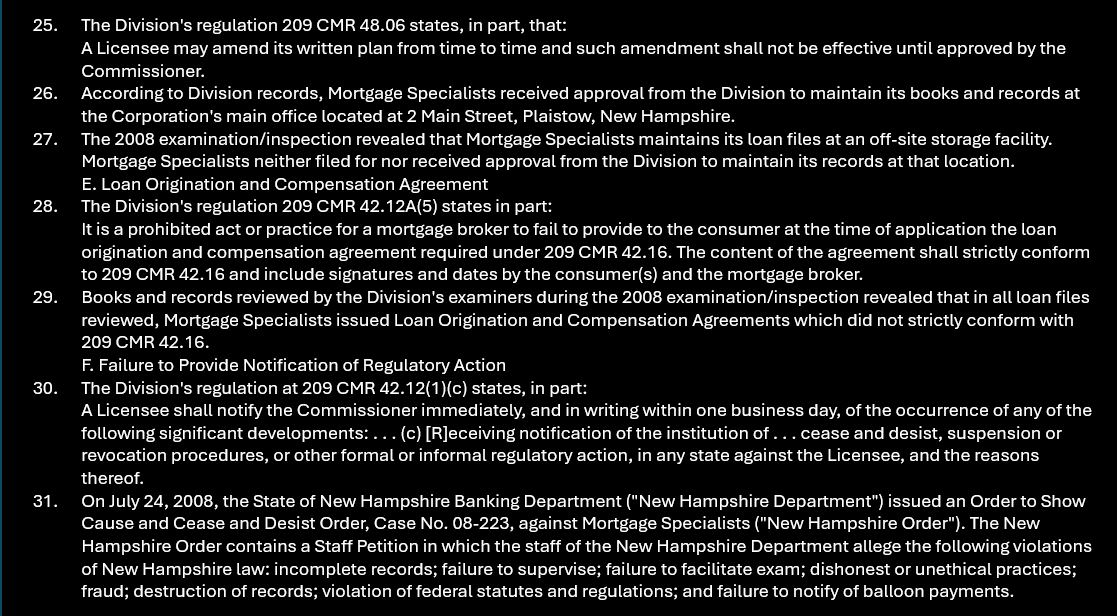

Mike provides his fantastical account in his 44 page Scribd full upload found here:

Mike Gill Report-44 | PDF | Divorce | Lawyer (scribd.com)

Trouble in Paradise

“Mike and Sarah had been having marital difficulties off and on for a few years. They went to counseling both as a couple and individually with Dr. Robert Broussard of Topsfield, MA first in late 2004 to early 2005 and again in the early Spring 2007. At one point, Dr. Broussard told Sarah and then Mike that he felt that Sarah suffers from Borderline Personality Disorder and that he would like to meet with Sarah on an individual basis. Mike spoke with Sarah and she confirmed the diagnosis. Mike would from that point on drop her off for therapy and wait in the car for Sarah.”

So, I can find zero evidence Sarah suffers from this, as a matter of fact what happens to the evidence ranks with “thee dog ate my homework”. Back to the story.

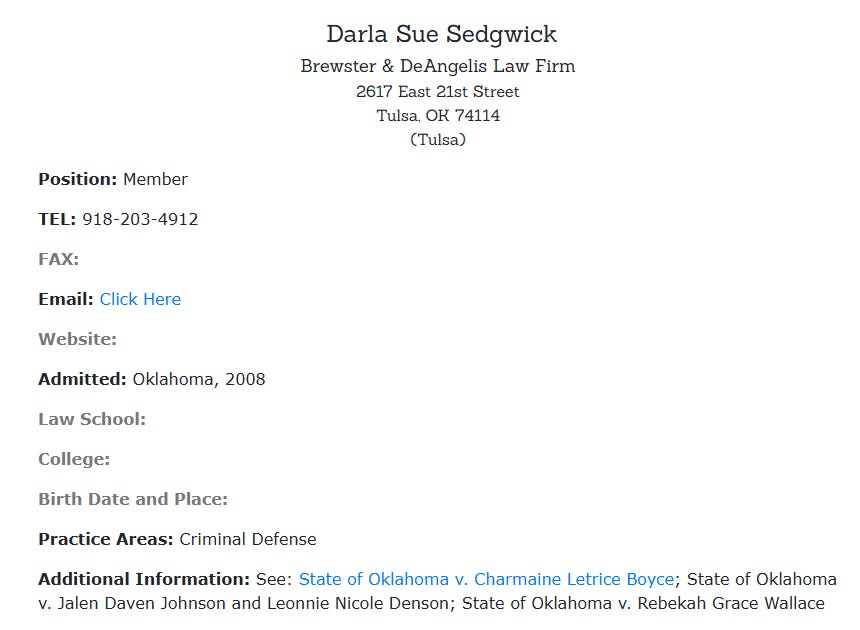

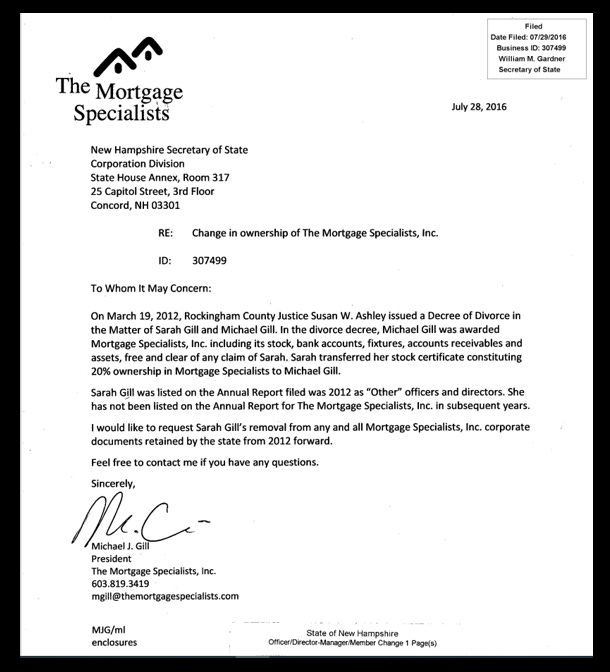

“In March, 2007 Mike's wife Sarah filed for divorce and was represented by Attorneys Ronna Wise and Matthew Kozol. Mike asked Walker for a divorce attorney and was referred to David Phillips of Devine. Sarah's attorneys challenged the representation, indicating a conflict because of Devine's representation of MSI (Mike was 80% owner, Sarah 20% owner). Walker indicated that there would be no conflict, but Attorney Phillips withdrew from the case in July, 2007 because of a conflict of interest. Walker then referred Mike to Attorney Jonathan Ross of Wiggin & Nourie and set up a meeting for Mike and Ross to meet. Darla Sedgwick, also of Wiggin & Nourie, filed her appearance as co-counsel on behalf of Mike in August, 2007.

From the beginning of the divorce action and continually, several different times during the course of the action, Mike offered to settle with Sarah. At this point, the marital estate was worth an estimated $60 million. Early in the divorce, copies of Dr. Broussard's records were requested by Mike's attorneys to be used as part of the divorce proceedings. A court order was issued ordering Dr. Broussard to produce the records. Three days later Dr. Broussard first responded that he no longer had them and gave three different reasons at three different times (fire, flood & accidental shredding) as to why they were no longer available.”

Let’s continue with his fantastical story in his own words…You can read the entire rambling 44 pages using the link section-header above. Sarah filed in March 2007, so we are moving forward about 11 months in Mike’s account of his divorce.

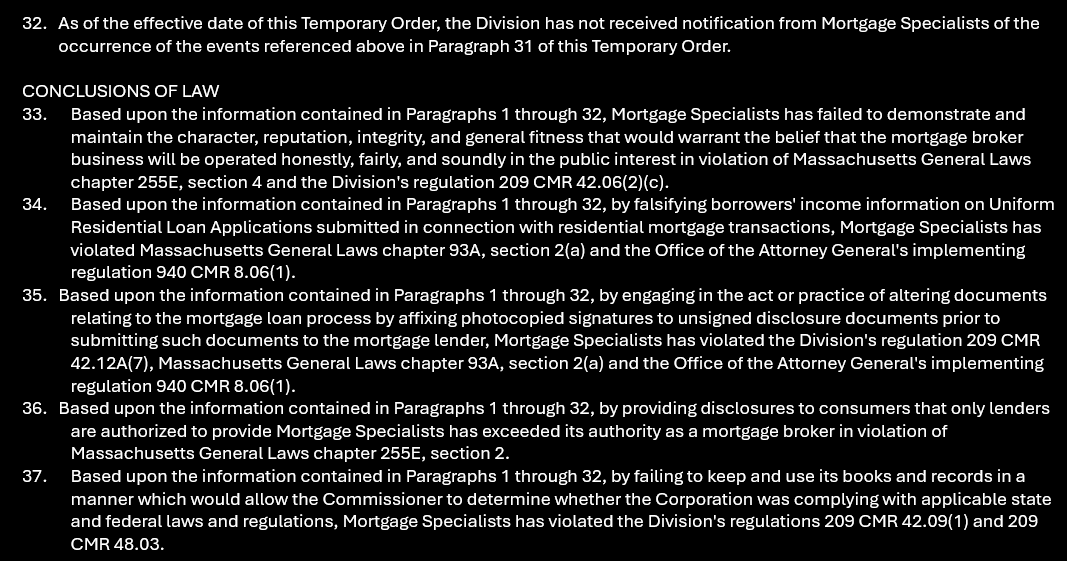

“In February, 2008, Attorney Stephen Tober filed an appearance as Sarah's divorce attorney. Attorney Tober and his law partner Tara Schoff were the attorneys who were brought in to begin pushing the cases beyond the statute of limitations.

I am sorry, I have to interject here as we are talking about divorce proceedings, he surmises Tobler had a nefarious role which was “pushing the cases beyond the statute of limitations”, what Statute of Limitations issue? This is a year into a divorce with minor children and he is trying to paint some grand conspiracy of victimization. So far, he has levied accusations against the therapist, the lawyers representing Sarah and those representing him. Okay back to Mike’s account.

In February 2008 Sedgwick had her paralegal, Megan Beauregard, research and prepare a motion to remove Tober from the case for a conflict of interest based on his prior representation of Ross, Sedgwick and Wiggin & Courie on previous cases as well as a close personal friendship between Ross & Tober. Ross refused to let Sedgwick present the motion to the court. While Sedgwick informed Mike that she had previously been represented by Tober, Mike was not informed until much later that Tober had previously also represented Ross, and Wiggin & Nourie. Mike was also never told that Ross and Tober have a very close personal relationship. They vacation together and have served on several committees together.

The Drives were Drilled?

About the same time as Mike found out about Taber's representation of Ross, Sedgwick and Wiggin & Nourie, he also found out from Dennis Stone of StoneTum Group that Sarah was seen in Tober's office months before he filed as her divorce attorney. Stone also told Gill that Sarah's computer hard drives had been drilled and were no longer in existence and could not be used as evidence in the Divorce case.

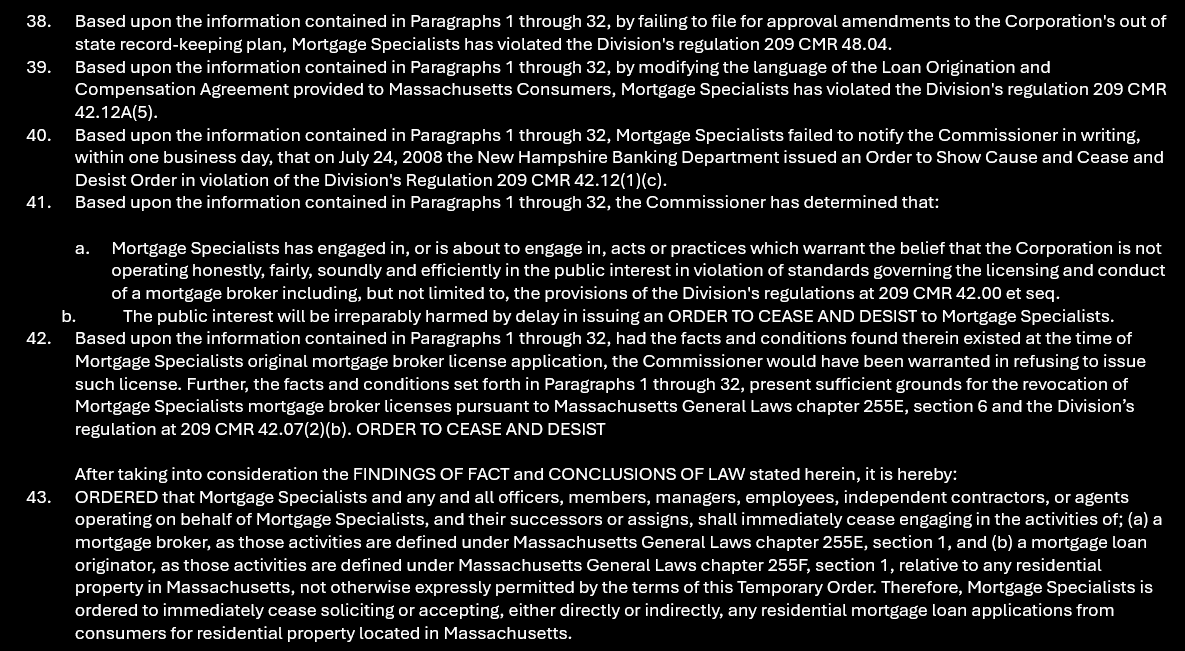

When Mike asked why they would drill the hard drives and Stone's exact words were "sometimes the sanctions are less damaging than what is on the computer." Stone was a witness and was at the hearing where the motion was supposed to be filed. Stone also told Mike that Tober had delayed filing an appearance in the divorce until there was resolution in a malpractice in which he was representing Ross.

“Later in February and April, 2008 Wisc and Kozol, respectively withdrew from the case, with no particular reason given, after billing more than $500 000.00. In hindsight it appears that Wise and Kozol were only involved in the case to get it started while Tober completed his representation of Ross, Sedgwick and Wiggin & Nourie (Mike's divorce attorneys).”

His wife’s hard drives were drilled, come on why? Who are these people, seriously. He bloviates another paragraph about not knowing about another conflict of interest by legal representation and picks up here.

Sex in the City

“April 2008 Mike and Sedgwick took a trip to interview a Psychologist (Marc Ackerman) as a potential expert in the divorce. It was at this time that they begin a sexual/personal relationship. Mike believed that the Controller for MSI had booked the trip for him and he found out after that Sedgwick took the credit card information and booked the trip for the both of them. He didn't know that Sedgwick was coming until shortly before the time. Once on the trip Mike found Sedgwick naked in his hotel room. Mike was emotionally vulnerable and upset about the effect the divorce was having on his children and Sedgwick was a sympathetic supporter. Mike broke off the relationship with Sedgwick after a brief time and she continued to pursue him. She sent him letters and cards of a personal nature and even showed up at his house drunk.”

I find this to be his most telling recollection, as it illustrates the inner workings of Mr. Gill’s thought processes. He sets the table by casting dispersions on the intentions and role of her firm in his divorce. He then tries to justify sleeping with his attorney, with claims of his emotional vulnerability. SLAM the brakes! We are barely into his claims and so far, EVERY person has been working together in this grand conspiracy against him in his divorce. So far, he has vacillated between accusations and excuses. He has not skipped slandering one person in his “recollections of the facts”, NOT one.

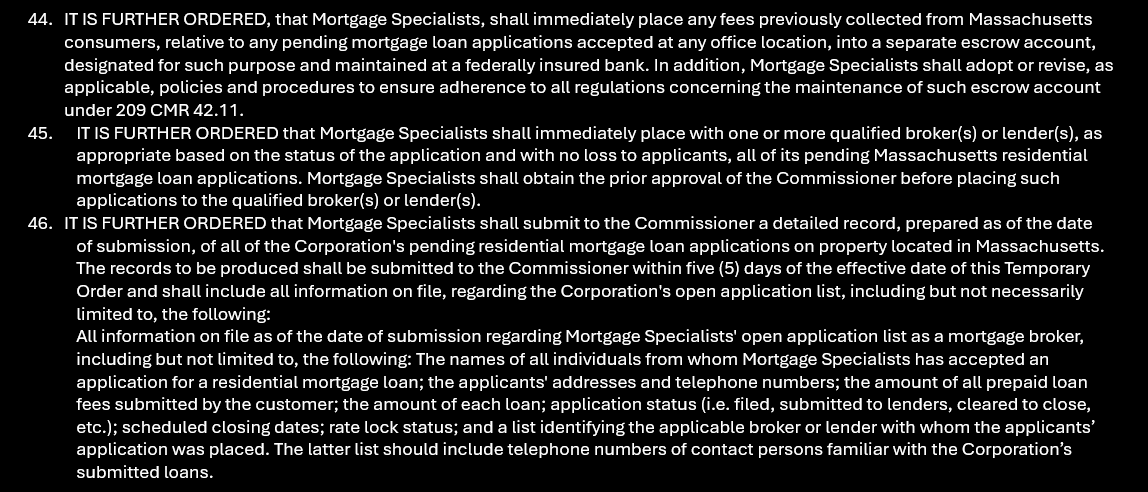

Does anyone else find it strange that the smartest man and the greatest fighter could be so duped in his divorce? To recap, it is 2008, and by his repeated verbal accounts, he left horse racing in 2006 at the top and he owns the biggest mortgage company in the country. That is why it appears the bulk of the NH Bar is in on a conspiracy with Mike’s estranged wife against him. Ok, back to Mike’s account.

Give the Gal Immunity!

“During this time in 2008 Mike told Walker about Sedgwick and expressed concerns that he didn't trust Ross. Walker was Mike's confident, and he confided in him everything about his suspicions and discussions with Sedgwick. Walker continued to tell Mike that there was no problem with Ross. Walker set up a meeting at Devine to discuss Ross and the potential conflict issue that Sedgwick had brought up.

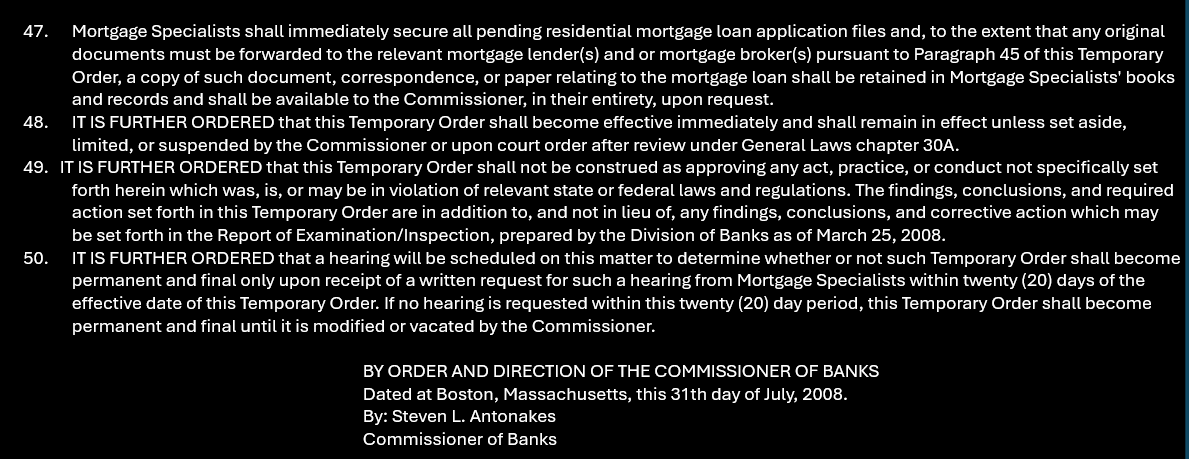

After the Devine meeting, Mike went to Sedgwick to discuss malpractice concerns against Ross. Sedgwick arranged a meeting with Lee & Levine in Boston MA and Mike. He was told by Sedgwick that the meeting was to address malpractice, but it was actually to discuss obtaining new counsel in his divorce. During the meeting, Attorney Levine strongly advised Sedgwick to obtain an Ethics attorney for herself after he expressed concerns over the personal nature of her relationship with Mike. At this meeting Attorney Levine gave Sedgwick the name of an attorney with professional ethics experience. Lee & Levine took a $50,000 retainer at the meeting. Shortly thereafter there was a meeting with Sedgwick and Attorney Levine at the 100 Club in Portsmouth Attorney Levine declined to become involved in the case and returned all but $7,500 of the original retainer. Mike was told by Sedgwick that Ross and Walker didn’t know about this meeting and that "Ross would shit himself'' if he found out.

Subsequently around June 2011 Mike obtained the itemized invoices from Lee & Levine which show that the initial call to Lee & Levine was from Walker. Sedgwick set it up with Walker and Ross's approval, but she told Mike that they didn't know. It was only later discovered by Mike that Lee & Levine are actually divorce counsel and that the whole meeting was staged. In May 2008, after the meeting with Lee & Levine, Sedgwick's relationship with Wiggin & Nourie began to break down. Shortly thereafter, Mike fired Attorneys Sedgwick and Ross. At that point not much had been done to resolve the divorce (no depositions, settlement negotiations or mediation had been scheduled). Sedgwick, under pressure and threats from Ross and Walker, moved back to her home State of Oklahoma. Sedgwick told Mike that she was so scared that she hired an armed guard to protect her. Give her immunity and she will tell you everything.”

Sleeping with the Enemy

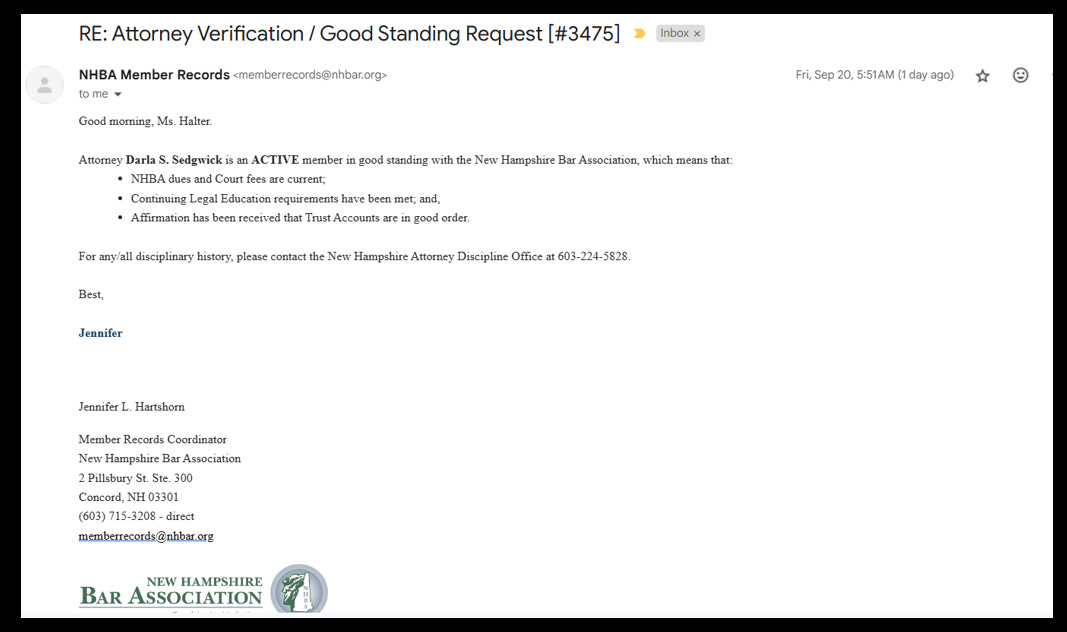

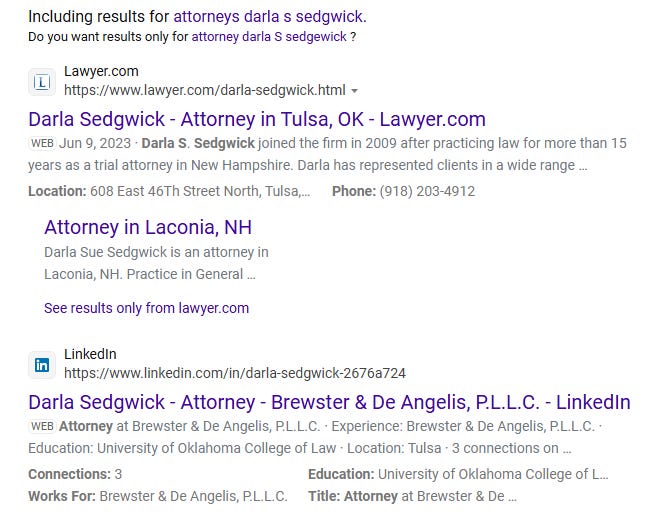

Wow! Love how he is the victim when sleeping with his attorney. Wow, just wow. Speaking of Darla what happened to her? Mike said essentially fled to Oklahoma and had to hire armed guards. I feel compelled to know what happened to Darla. Is she ok, I thought I probably would not find her, because surely, she is in hiding. I checked with New Hampshire and Oklahoma and voila! She doesn’t need immunity, there is nothing to tell. She is a reputable attorney that made a mistake with a mentally unstable client in a divorce proceeding. She was undoubtably embarrassed by her huge mistake; however, she is still actively licensed in NH as well as OK and in 2018 was the Assistant County Attorney for Belnap County, NH.

My email response yesterday below.

BING SEARCH RESULTS

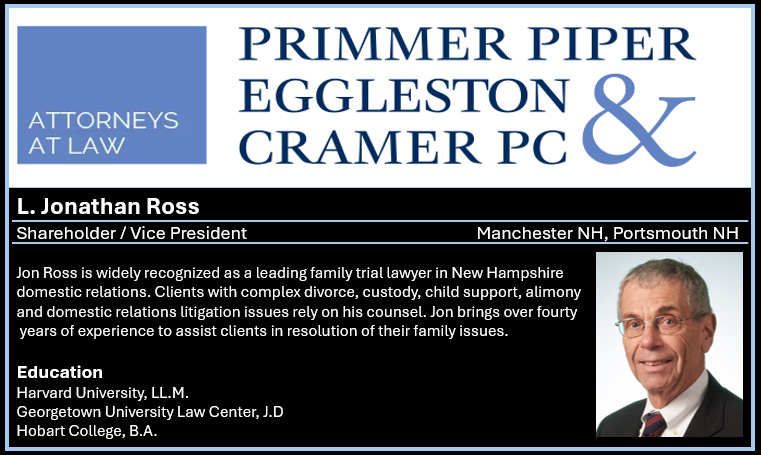

It would appear to me, Darla did not go back to Oklahoma to hide, maybe from the shame of sleeping with a client, a client no less with a strong penchant for slander. What about “Ross”, after all Mike had to fire them; they were Walker’s pawns, at least that is what Mike would like us to believe. Ross was the President of Wiggin and Nourie, when this occurred where he remained until he and others joined Primmer, Piper Eggleston Cramer PC.

By Staff | Feb 1, 2012

MANCHESTER – The confluence of an unstable economy, a tightly competitive legal market and an ongoing exodus of more than half its lawyers since 2010 all contributed to the decision to close down Wiggin & Nourie, one of New Hampshire’s oldest law firms, its president said.

The law firm, which was established in 1870 under the name Burnham and Brown, informed employees Thursday that it would close its Manchester and Portsmouth offices. Clients are still in the process of being notified of the closing.

NH Pro Bono Program Recognizes Jonathan Ross for Lifetime Achievement

10/2020 - The New Hampshire Pro Bono Program recognizes Jonathan Ross for lifetime achievement. Jon has spent the last 52 years of his career doing and promoting pro bono in New Hampshire and nationally. Justice Gary Hicks describes Jon as "An inspired attorney who puts the law above himself." At our firm, Jon serves as a mentor to many and a constant reminder that being an attorney is a privilege and challenges his peers to do more. Although this award may indicate that Jon's work is done, he is far from finished. Jon will continue to serve families with complex divorce, custody, child support, alimony, and domestic relations litigation issues for many years to come.

Well on the surface I see nothing nefarious with Mr. Ross. In a 2014 State of Corruption Press Release, Mike references a case involving Wiggin and Nourie v Michael Gill V L Johathan Ross and Darla Sedgwick, docket number 218-2011-CV-591, however other than Mike’s “press releases” and references I cannot find it. He claims in 2014 press release that the case is ongoing, however Wiggin and Nourie ceased to exist April 1, 2012. Because it is not listed with the court, it is safe to say it was or dropped/withdrawn.

Back to Mike’s Divorce Recollections

In June 2008 Mike and Walker met with Attorney Jim Tenn of Tenn & Tenn. The first thing Walker said in the meeting was "I am not going to sue Ross". No one asked him to. Walker said this in front of Tenn, as his way of subtly intimidating Tenn into conforming with the plan already in place. Mike now believes that the plan the entire time was for the attorneys involved to drag out his various cases in order to allow the statute of limitations for filing malpractice complaints to expire. Mike was already beginning to suspect that Walker was protecting Ross, and this statement further confirmed it. Mike found much out later that Ross and Sedgwick had a meeting with Tenn prior to his meeting and without his knowledge.

In June 2008 Tenn filed his appearance to represent Mike in the divorce. At this time Tenn decided that the case needed "some grey hair" and hired Attorney David DePuy ("DePuy") to be co-counsel. Tenn represented Mike from June 2008 to May 2009. It should be noted that DePuy was Tenn's mentor. DuPuy personally was on his 3rd divorce and was financially strapped. He was worried about not billing enough getting fired. DePuy was billing Mike 45,000.00 to $50,000.00 per month. The only way that he could have billed this much money (based on his hourly rate) was if he was billing Mike for every hour of every day of the week. When DuPuy was questioned about the bills, he suggested putting $2 million in an escrow account to bill from. Mike has a copy of the request in writing.

Mortgage Minute Timeline Update 2007-2008

Everything is a potential lawsuit, everyone is suspect, he slanders everyone and inflates numbers like a politician or huckster. Thankfully, during 2001 - 2007, mortgage underwriting standards declined significantly as did documentation requirements. In 2007, automated underwriting (no proper review) was responsible for 40% of all subprime loans. “Mortgage brokers, despite profiting from the housing loan surge, have failed to adequately assess borrowers' repayment capabilities. Consequently, mortgage fraud perpetrated by both lenders and borrowers surged dramatically.” - Mortgage Bankers Association Chairman 2008. Add the crazy points being paid and like all subprime mortgage mills he profited handsomely.

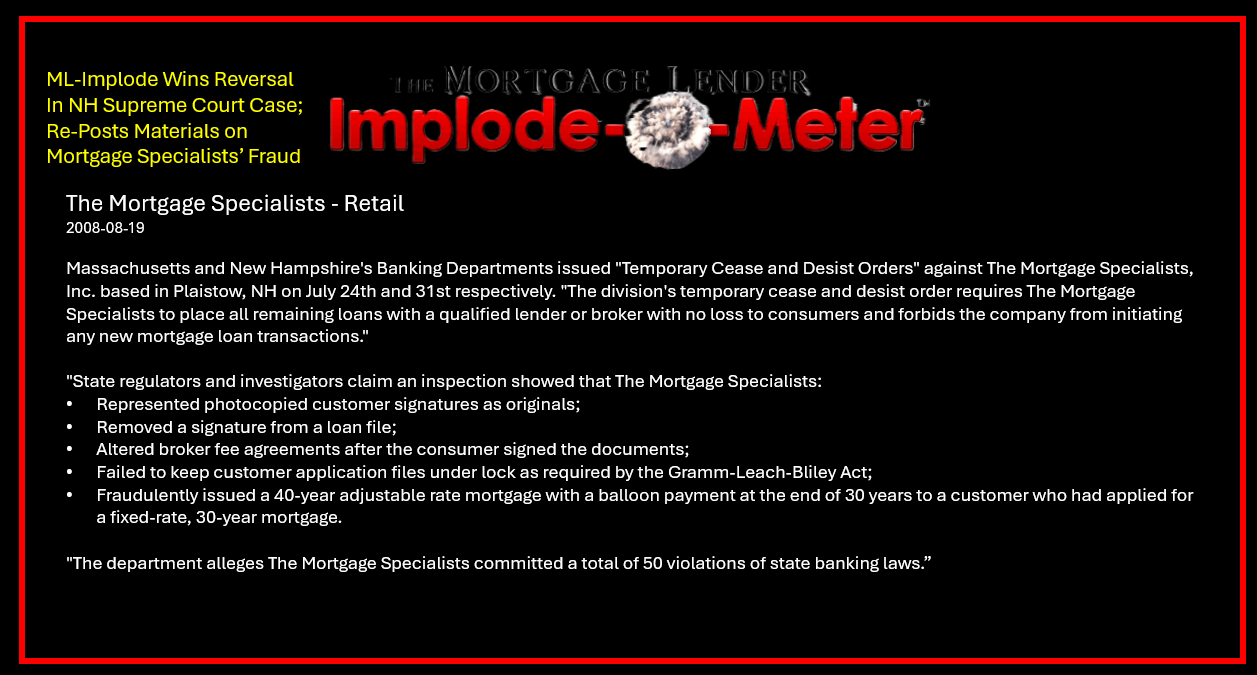

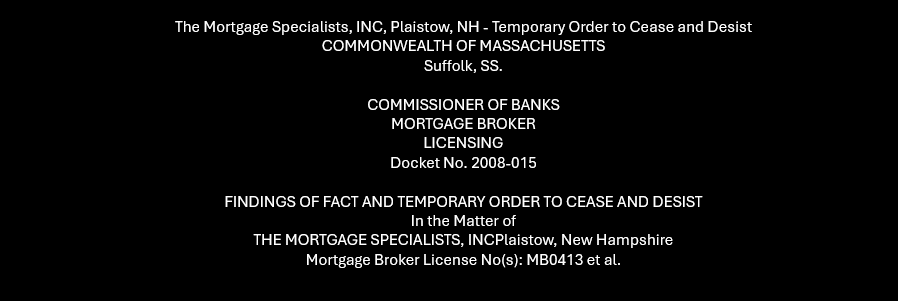

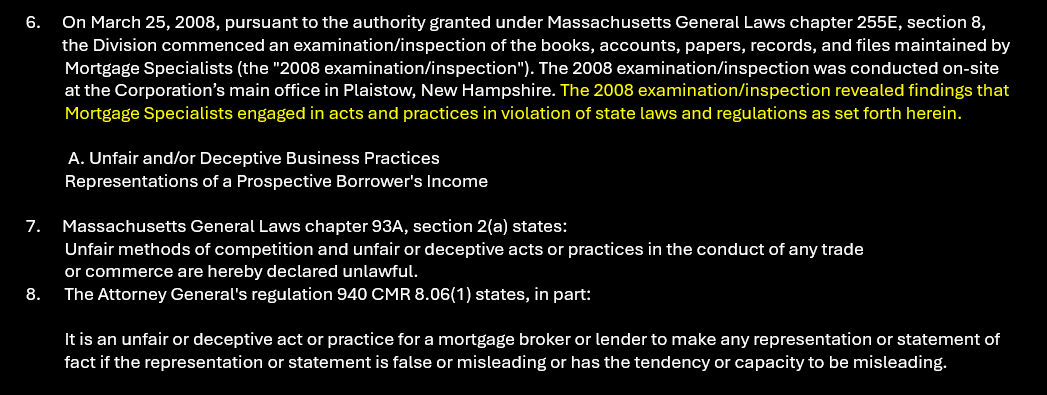

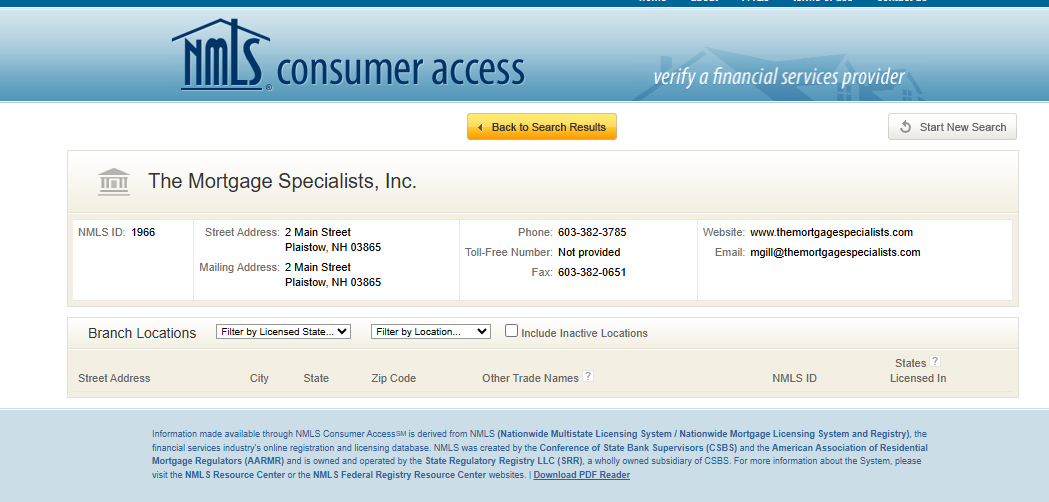

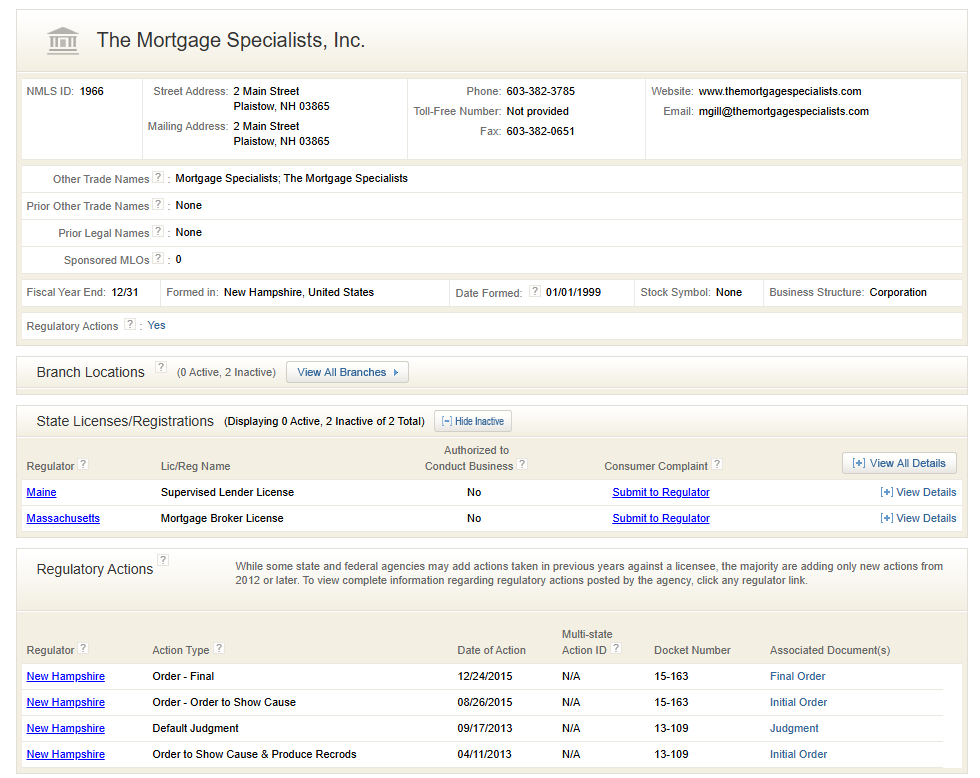

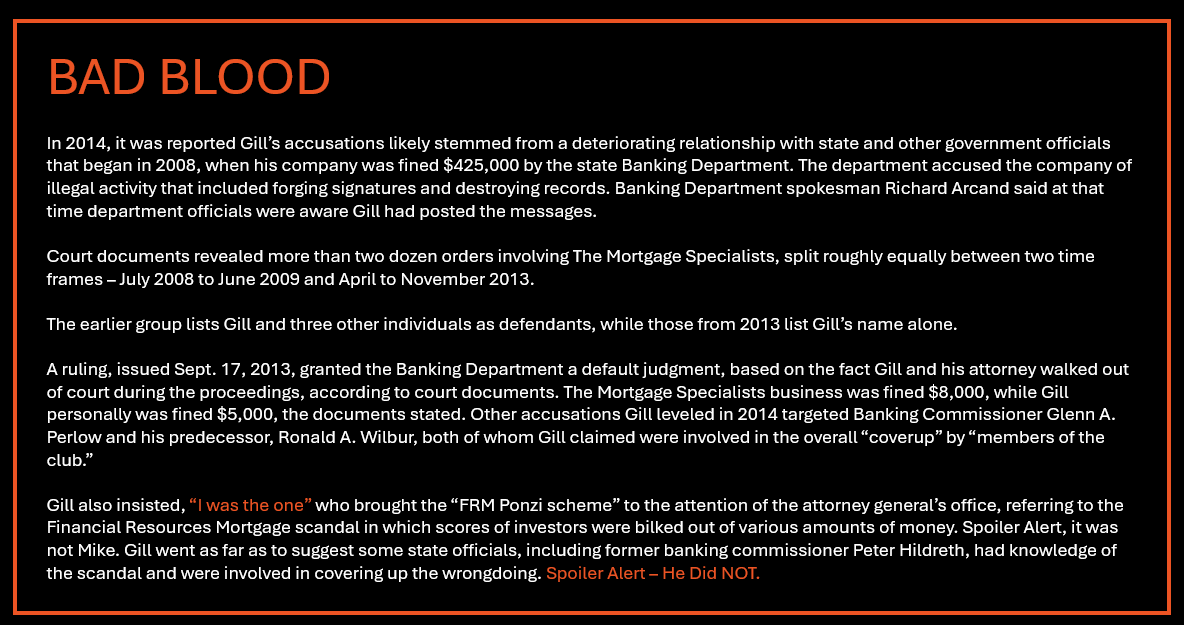

However, trouble she is a brewing. Mike’s Mortgage company’s 50 Violations of state banking laws was published on Implode-O-Meter in 2007 and of course he brought more lawsuits.

This was followed up shortly by more trouble with State Banking.

New Hampshire Fine: $425,000.00 Massachusetts Fine: $300,00.00

Cease and Desist ALL Mortgage Activity!

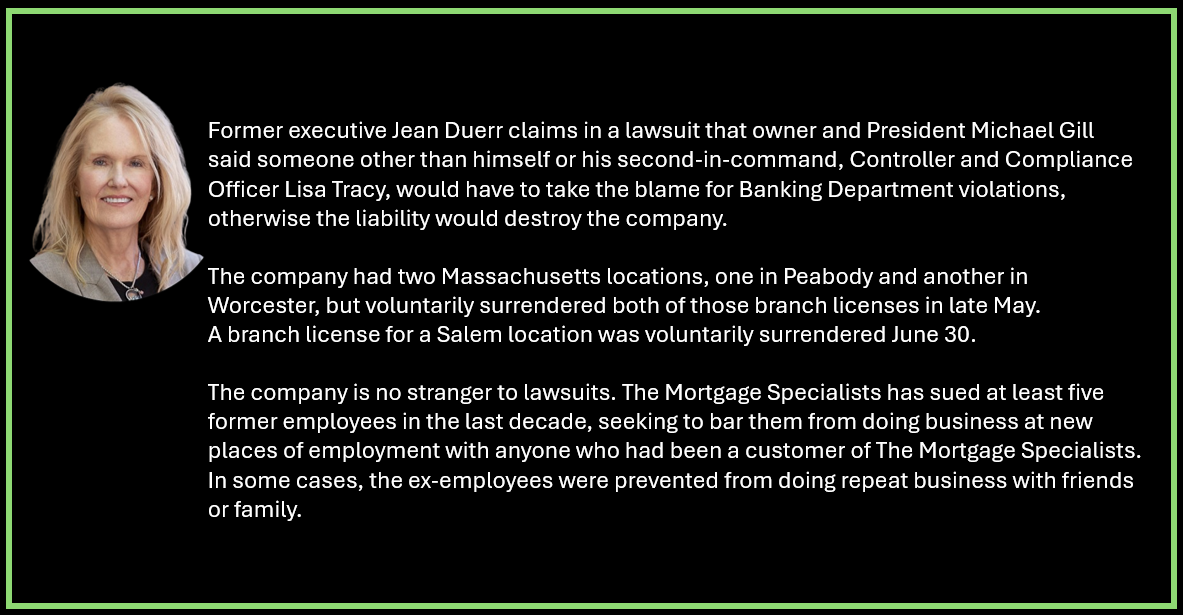

This is yet another illustration of how he does business. He was granted a license on appeal just 6 years ago on the condition he would have a compliance officer. Then this? This is a predatory lender. If you are old enough and worked under the financial services umbrella you see it clear as day. His infractions are predatory, lack of disclosure of balloon payments, falsifying income, forging disclosures, originating refinances and placing proof of beneficial interest on the borrower, and my favorite maintaining records offsite. This man is not a victim, but a victimizer.

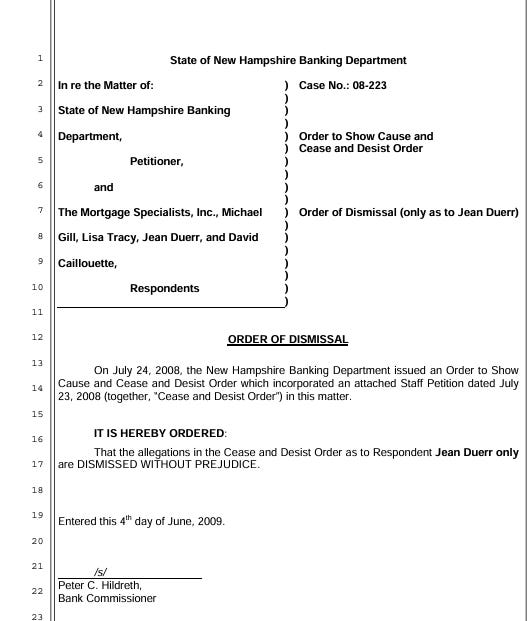

Jean Deurr cooperated with State Banking and was able to salvage her career post her Morgage Specialists Employment.

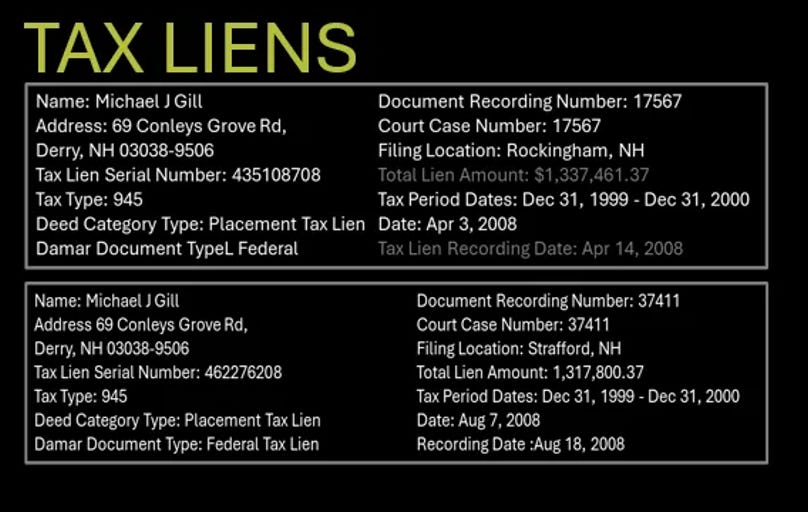

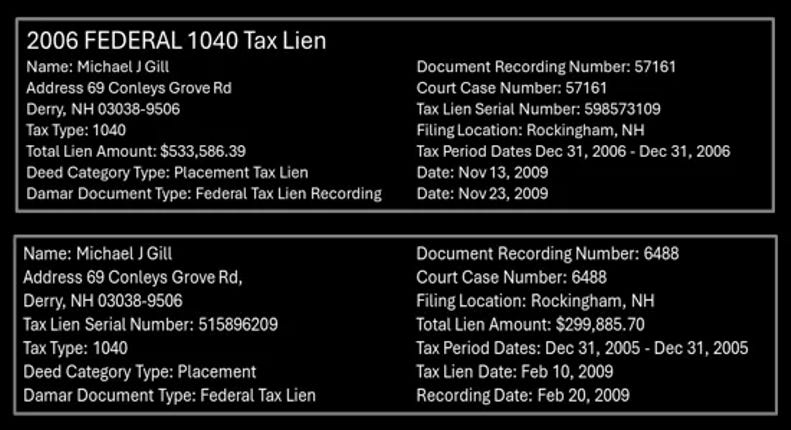

Liens, Lawyers, and Woes Oh No

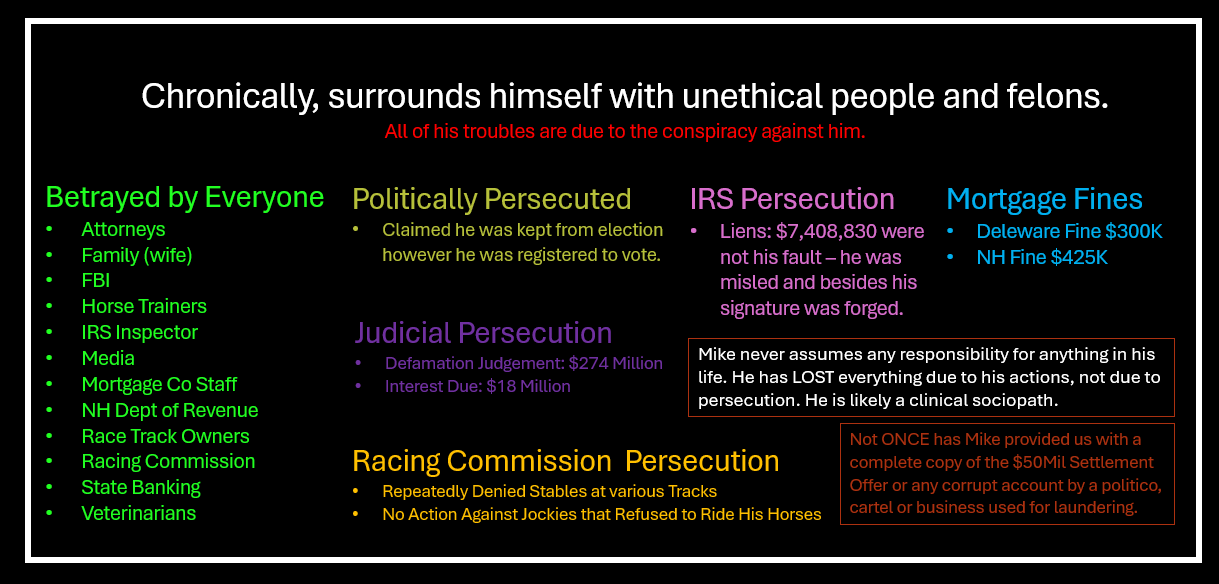

Mike’s tax woes are mounting, but of course it’s not his fault. However, in 2008 two considerable six figure federal tax liens are levied against Gill followed by 2 more in 2009. As you can see below, he hasn’t paid 2006 either, they just haven’t placed liens yet.

Let’s hear Mike’s “recollection”.

“Mike and Sarah Gill ("Sarah") begin filing separate tax returns in 2008 for tax years beginning 2005. Prior to that, Sarah's friend Joseph Faletra ("Faletra") prepared and filed the personal and corporate tax returns with help from Sarah, in fact, Sarah worked with Faletra preparing the business expenses and the depreciation schedule for the horses for Mike Gill Racing.

In 2006, the IRS issued a notice of tax deficiency for 2001-2004. Mike and Sarah were represented by Williams and Connolly, CCR, LLP and Devine. Subsequently, during the divorce, Sarah was represented by Justin Holden. Sarah claimed innocent spouse in the IRS case and later in the divorce action.

The IRS issues began to arise when Walker referred Mike to CCR LLP as accountants.”

Grant Thornton later on purchased CCR LLP and CCR would have been obligated to disclose any wrong doings to Grant Thornton. Walker's cousin Bill Tarzia, was a partner with CCR. It was Lawrence Schwartz ("Larry") also a partner at CCR who took the lead on the tax work for Mike and MSI. Larry worked closely with Maurice Gilbert, Jon Sparkman and Walker both of Devine. Gilbert worked for the DRA as a Manager for 25 years. He was then hired by Devine and began working on Mike's case. Gilbert knows everyone in the DRA and Mike believes that he is the one who controlled the DRA piece inside the DRA for Walker. The trouble with the IRS began when information regarding Mike Gill Racing was intentionally incorrectly filed with the IRS. Several forms including a K-1 and Net Operating Loss (" OL") form were fraudulently prepared by the tax preparer (counseled by the attorneys) and filed by Michael Gill.

Gilbert was the one that spoke to the accountants to have the tax returns adjusted assuming Mike would take a settlement. But the settlement came with a leveraged $28 million on my K-1 form making it New Hampshire Income. Even though this was argued with the IRS calling the horse racing not a hobby but a business and Mike won Schwartz left the K-1 issue for Walker to fix. Once Schwartz was fired he sent the information to Marc Cohen ("Cohen") of Cohen+ Associates. Cohen called Mike and told him that Schwartz had dropped off the information. Cohen asked Schwartz directly about the NOL mistake and Schwartz had no response. Cohen also asked Schwartz about the issue with the K-1 when Schwartz and Walker were the one who argued the case for Mike and won. Schwartz then told Cohen that he had been instructed by Walker to put the information on the K-1 and that Walker would take care of the NH DRA. The information was put on the DRA to provide Walker with leverage against Mike and to legitimize the issues with the DRA release for Walker and was rejected by Mike.

Gilbert called the accounting firm of Berry Dunn. They refused to complete and file the taxes because the way Walker was requesting them to be completed was fraudulent. Schwartz ended up preparing them instead. Berry Dunn called Lisa Tracy, the controller of MSI and indicated that Gilbert had previously told them that MSI had settled.

His responsibility was to screw up the NOL carry-back. It cost Mike close to $1 Million. It was a mistake that a junior accountant would not make. When the IRS began sending notices to correct the error, Larry did nothing. Schwartz also intentionally put thus putting leverage on Mike. Mike has now filed a criminal complaint with the IRS stating all of the facts. This was filed by Anthony Augeri. He intentionally screwed the complaint up. When it came to settling the IRS issues, Timothy Powell ("Powell") was the settlement agent on the case. When the settlement was presented to Mike, he was given less than a day to think about it and was told that Powell was retiring that next day. Three years later, with the IRS issues continuing, Mike found out that Powell had not retired and was in fact still the agent working on the issues surrounding Mike's tax returns.

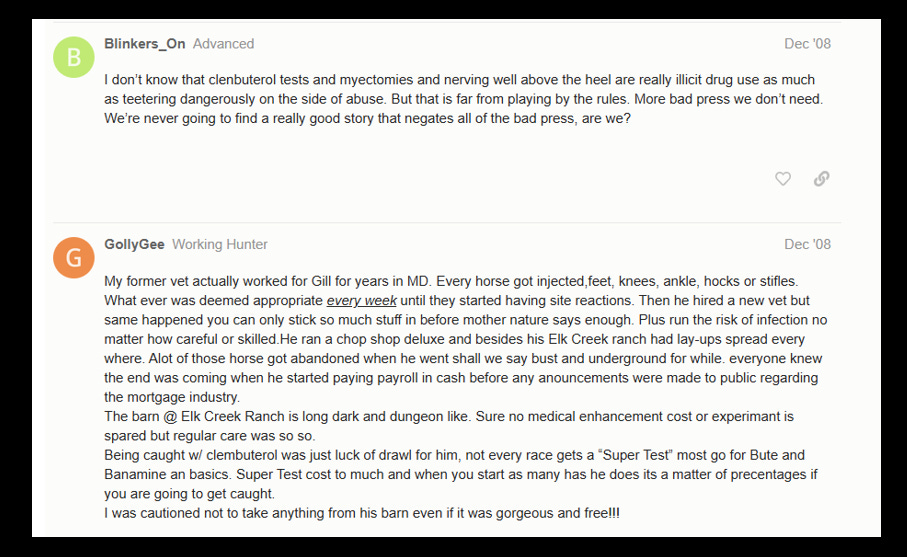

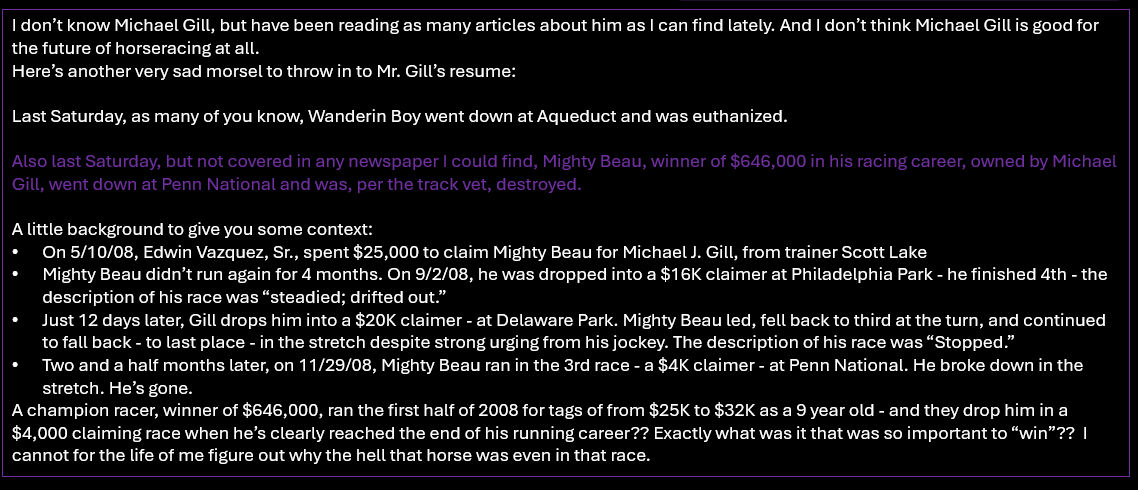

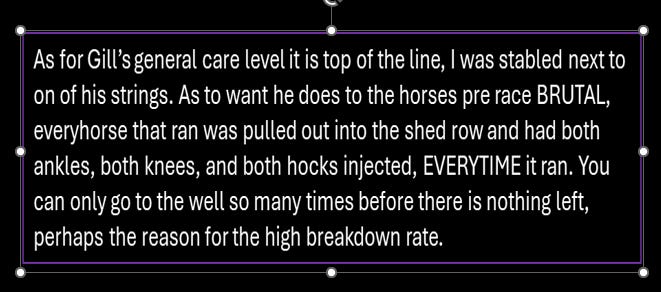

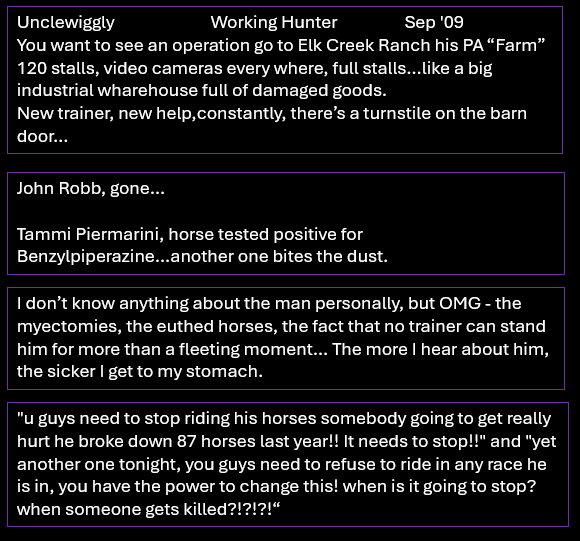

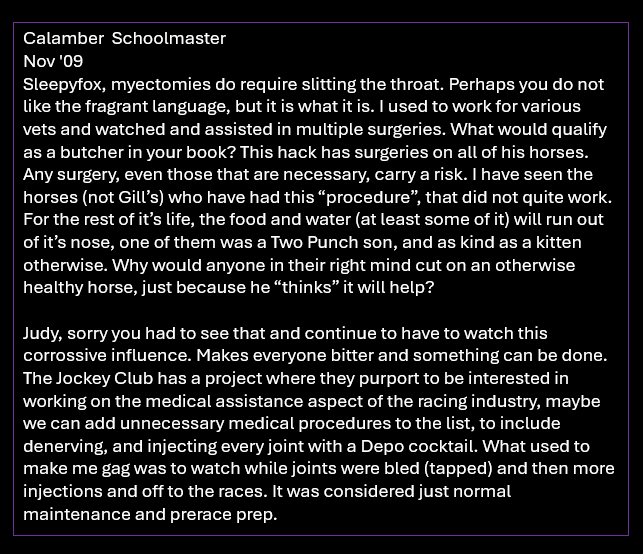

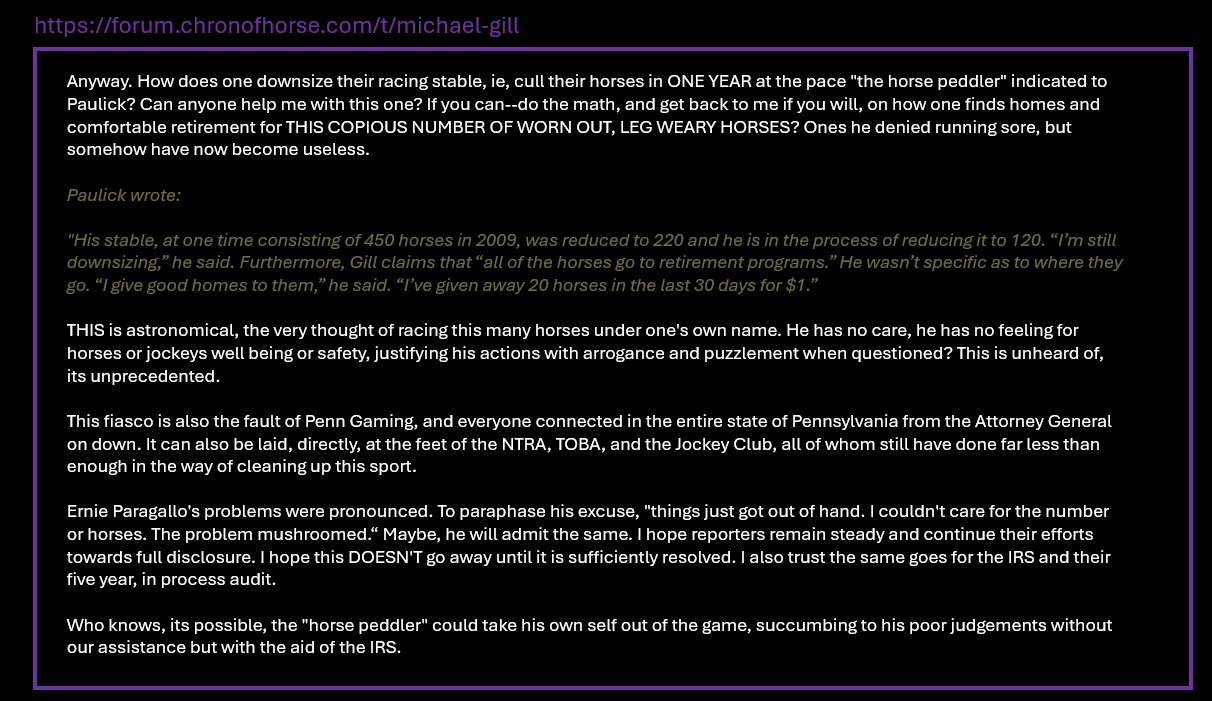

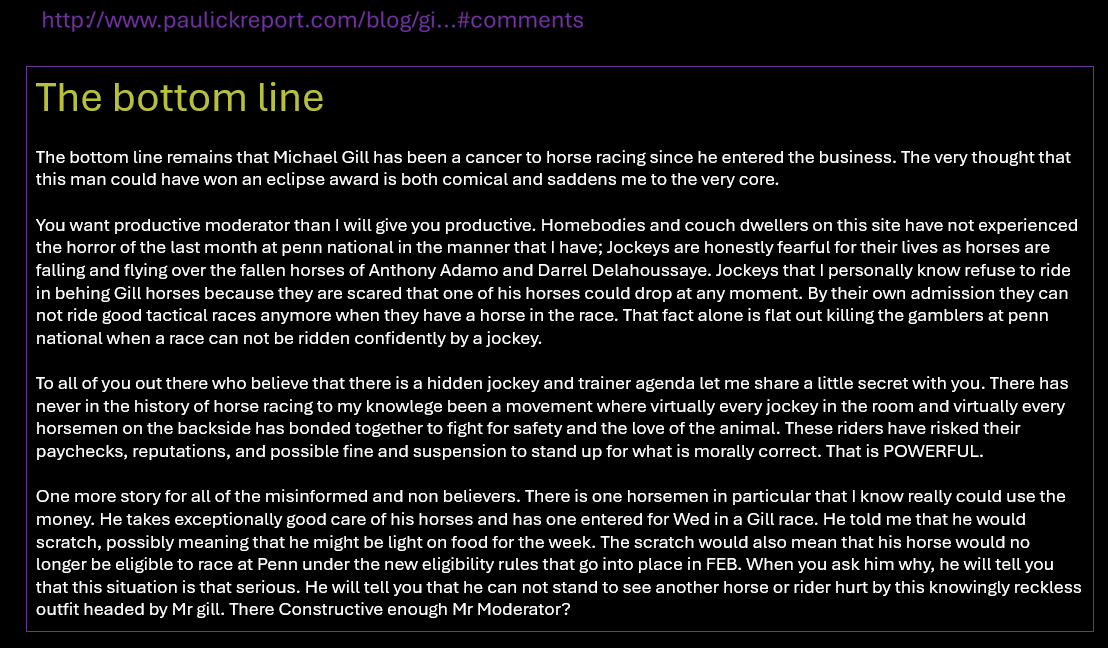

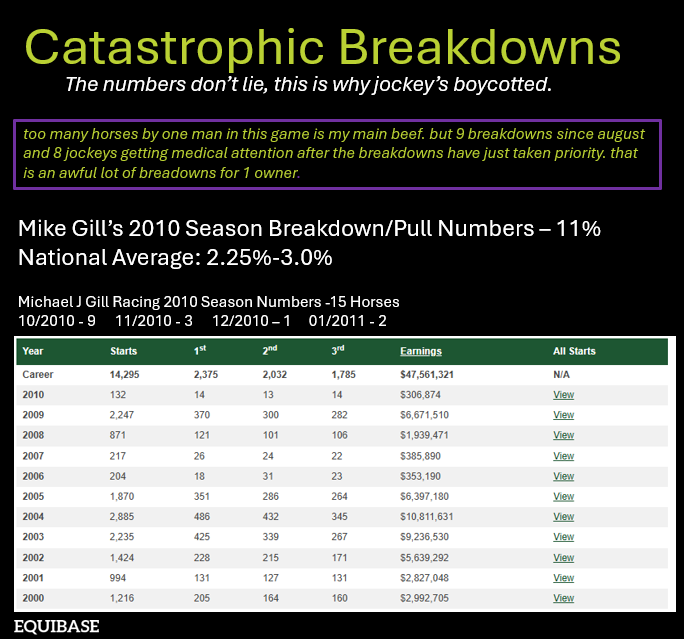

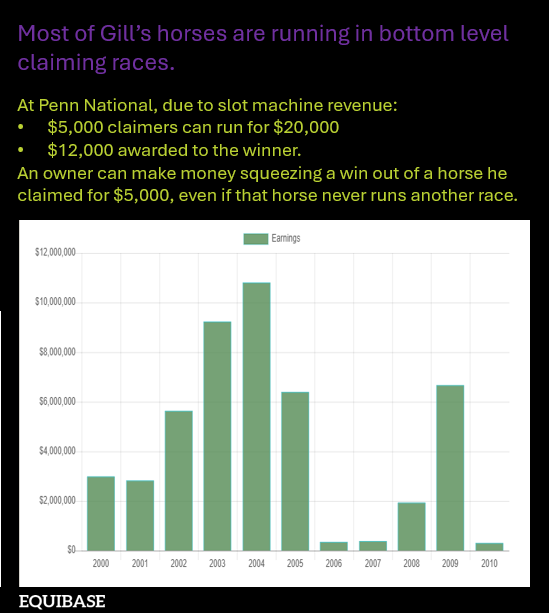

I am going to skip the commentary for above, other than to say YIKES. His mind is very busy. Meanwhile in horse racing things are not without controversy, conspiracy, insurrection, and yep, more lawsuits. Let’s see what is brewing, these are industry folks’ comments on https://forum.chronofhorse.com/t/michael-gill.

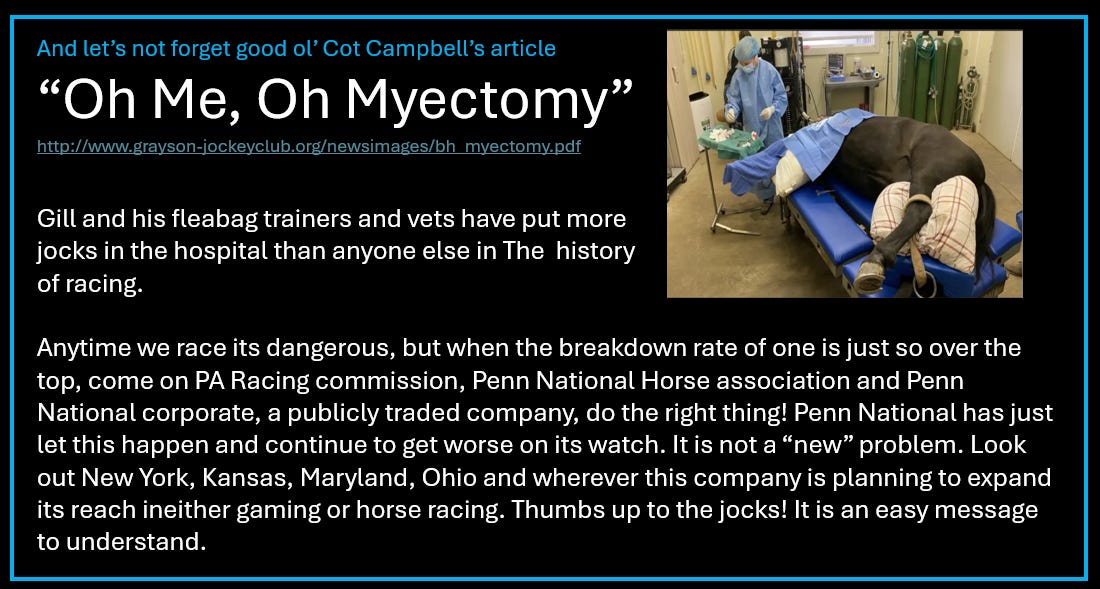

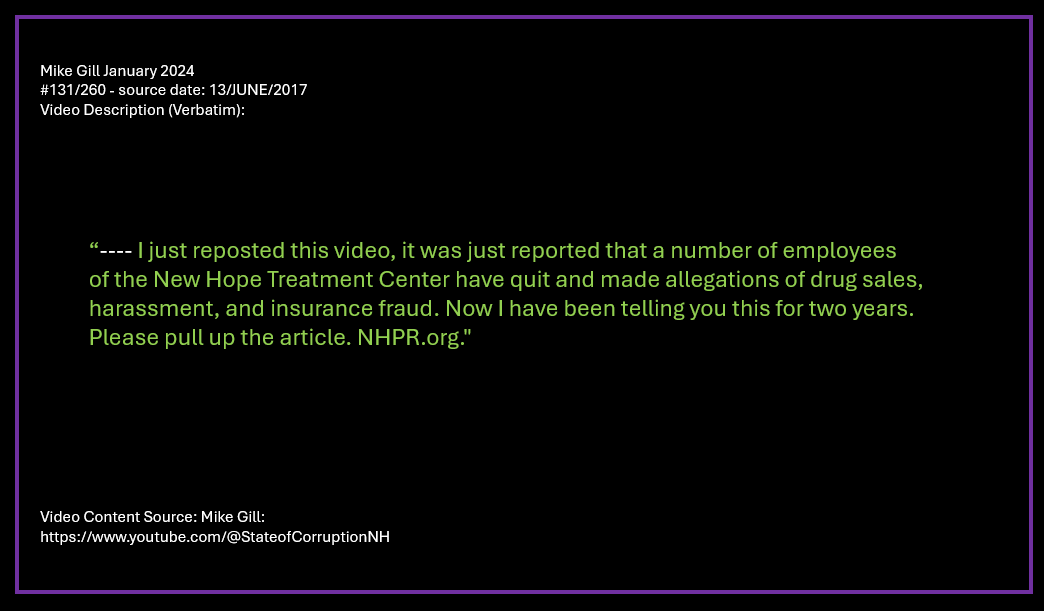

DRILLING HORSES INTO THE GROUND

The Paulick Report checked the references of this Elk Creek Ranch whistleblower, confirming as many of the details provided as possible. We feel confident the information provided is accurate.

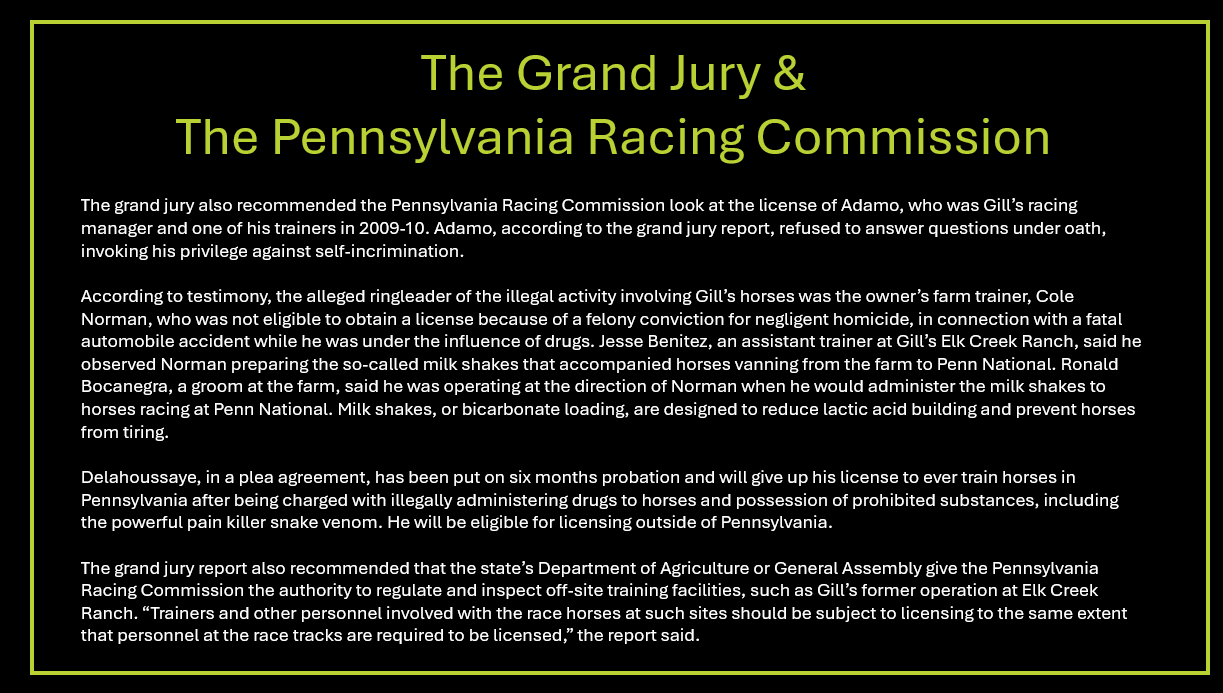

Adamo, this individual said, is often the one who does the injections of hyaluronic acid and/or cortisone—a contention Adamo disputes. “Tony only does the upper and lower knee joints and the ankle,” the whistleblower said. “He doesn’t do anything behind. He probably would if he had more experience.”

According to an individual at one time employed at Elk Creek Ranch who spoke on the condition of anonymity, Gill’s horses have been “drilled into the ground” since the arrival of Cole Norman as the farm’s trainer last summer. “Cole is set in his ways,” this person said. “He trains the crap out of them. They breeze every seven days (track condition permitting). They tap the joints of the horses, sometimes right after a race, and they tap ‘em every week, again and again and again if they don’t get sound. They are going to the well too many times. You are not supposed to tap a lame horse.”

The Company He Keeps

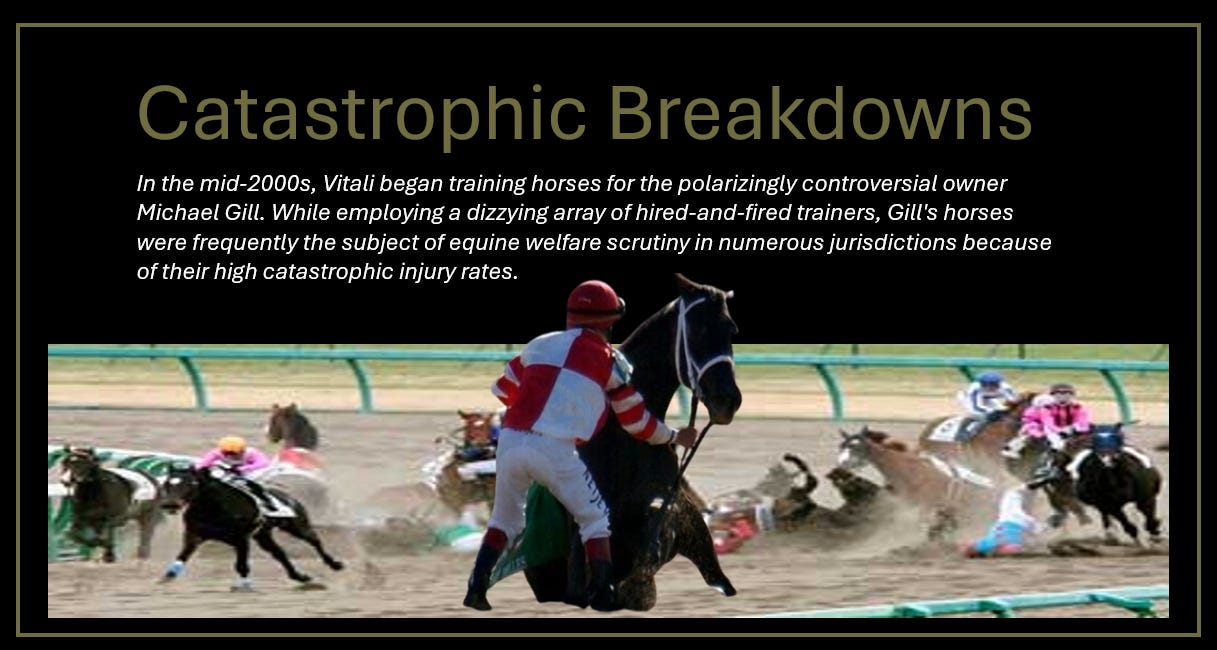

Mike rolled out as a trainer with his first horse failing for doping, serves a 3 year suspension and comes back and has a laundry list of doping docs and trainers. He has a couple that also have murder convictions (human not equine).

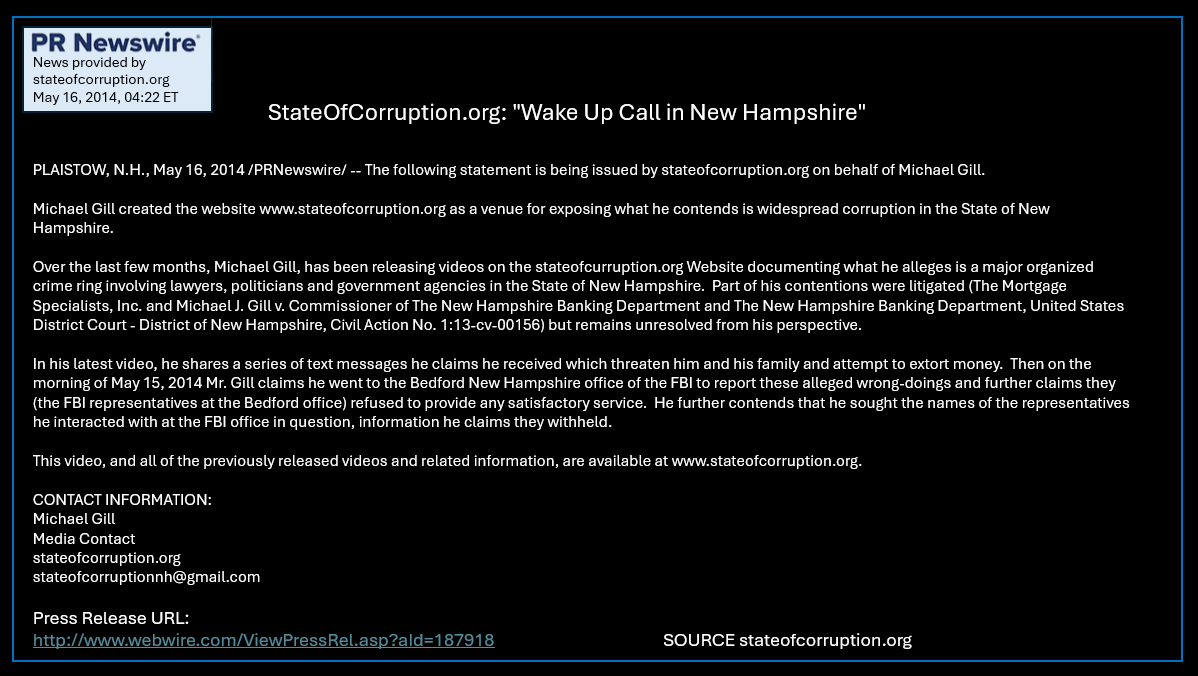

In 2014, Mike takes to the internet and the airwaves to air his grievances as the Judges in the suits he has been involved in and are not allowing Mike to deflect from taking responsibility for his misdeeds. The State of Corruption is born.

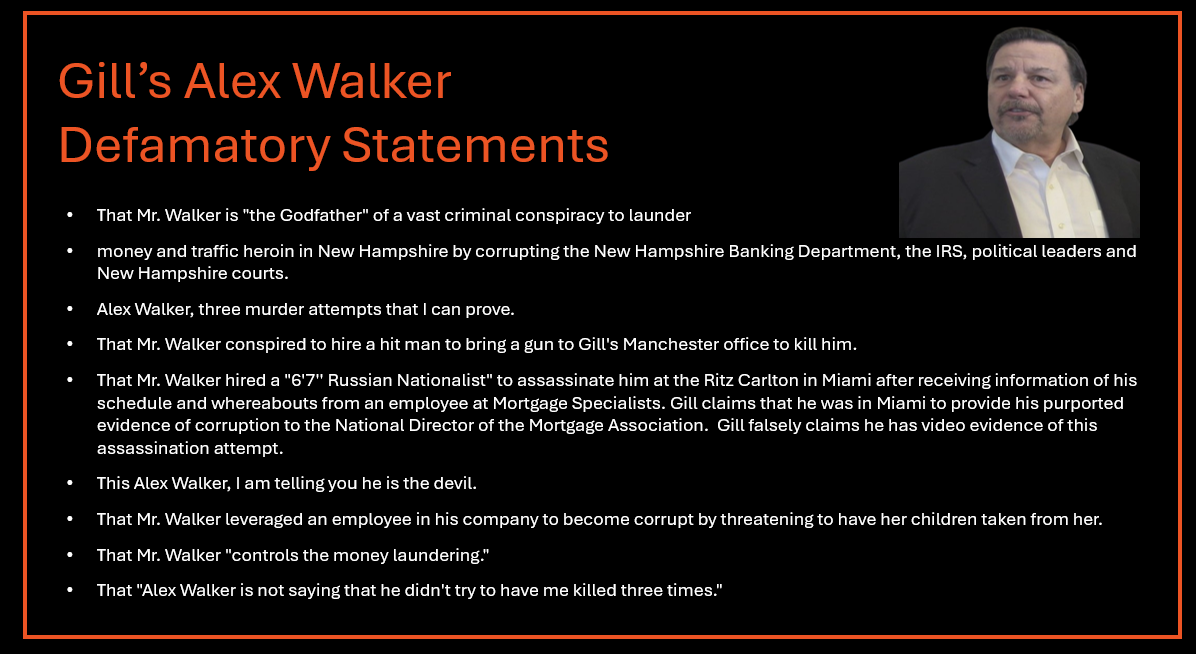

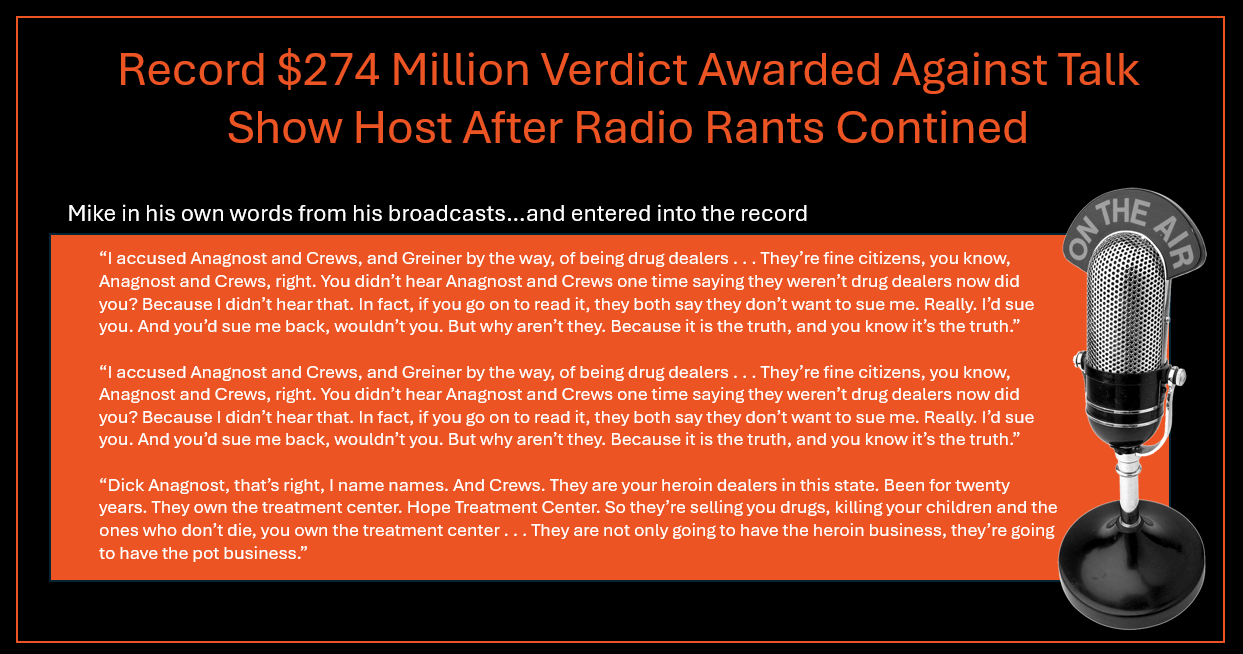

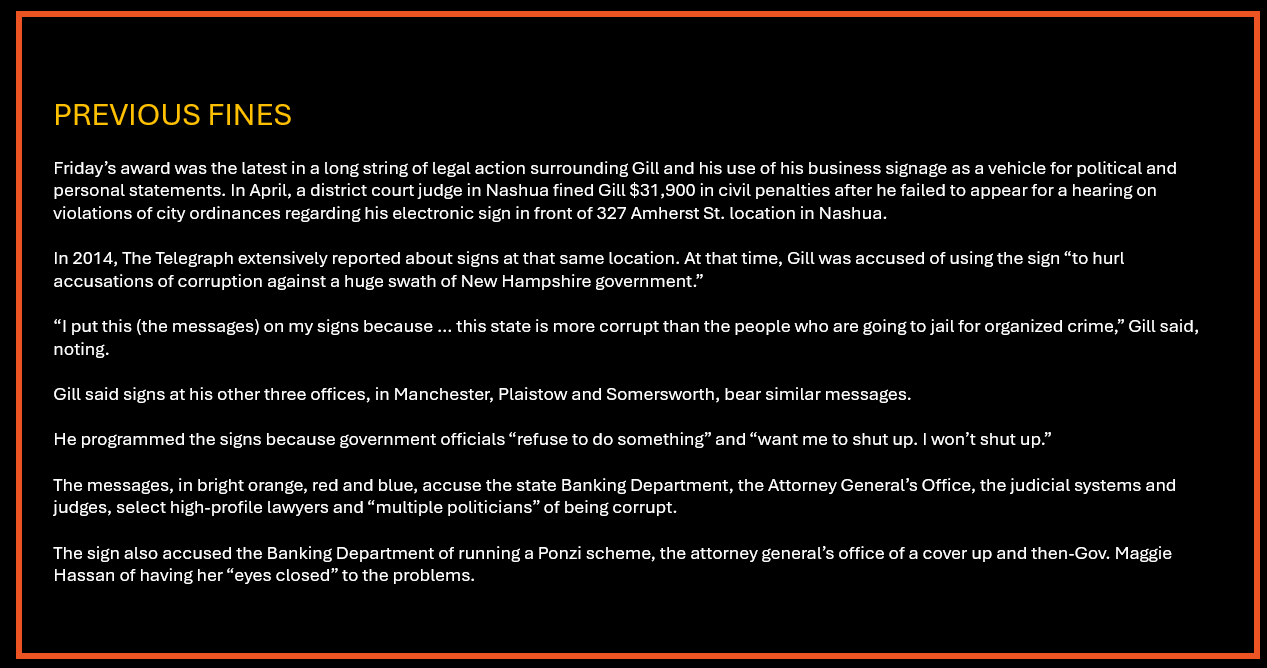

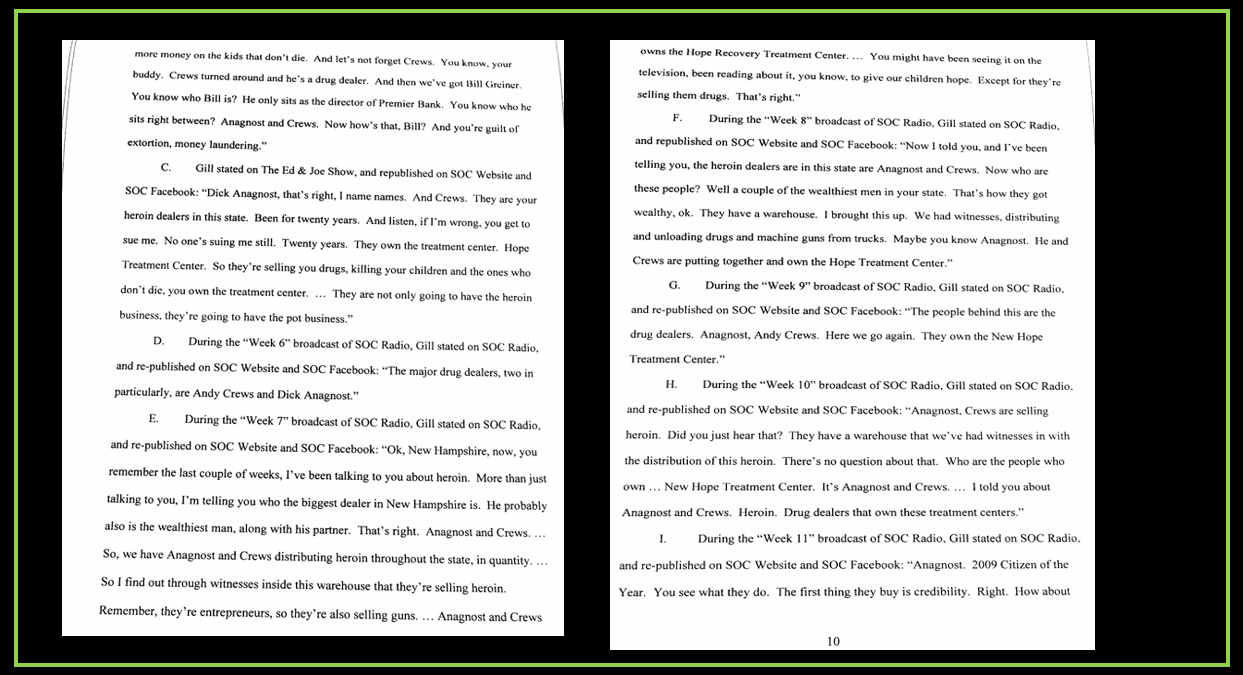

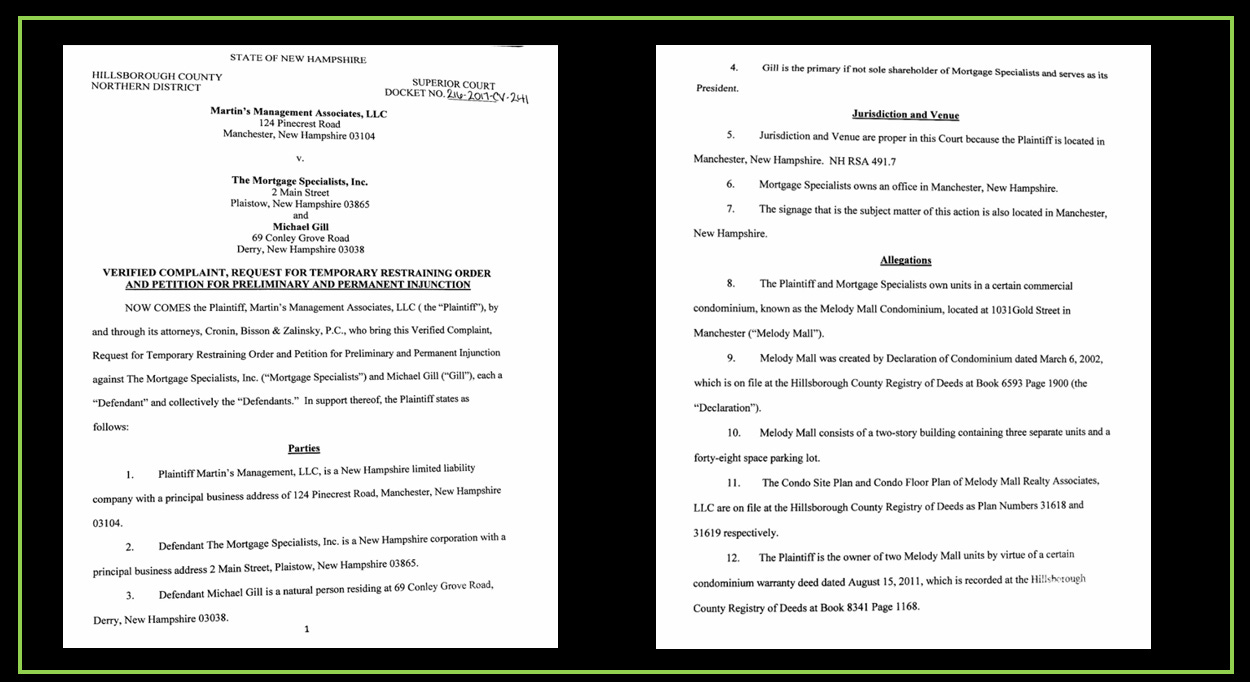

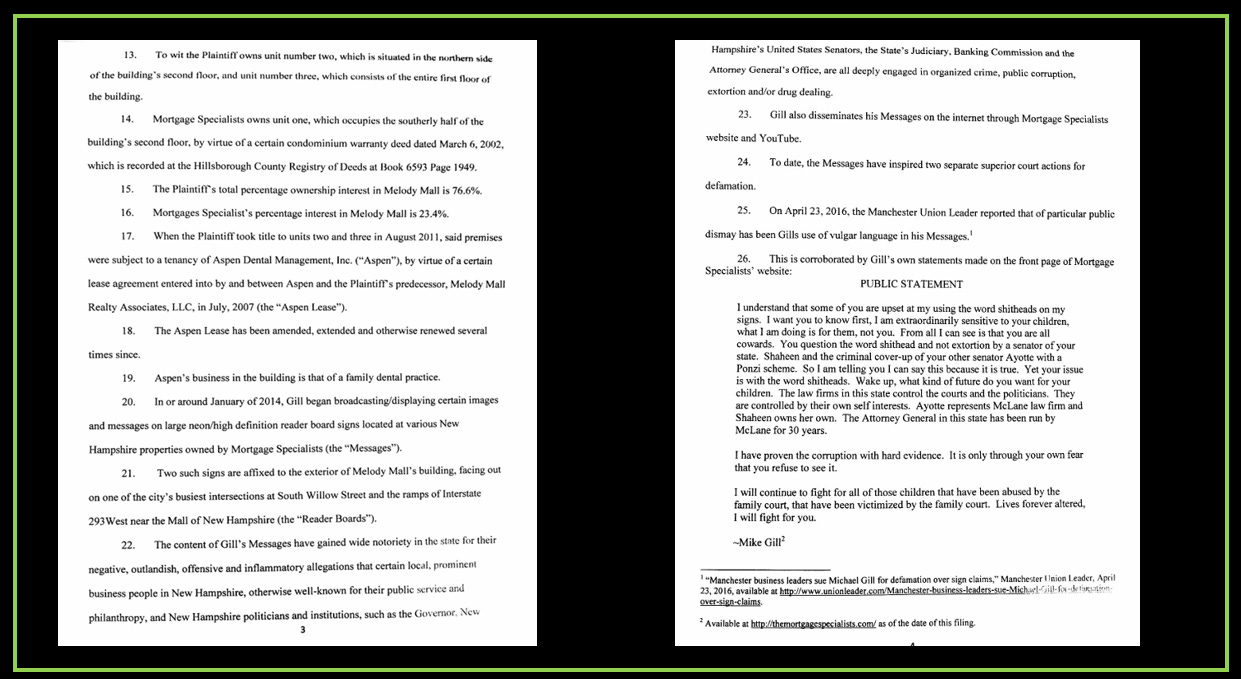

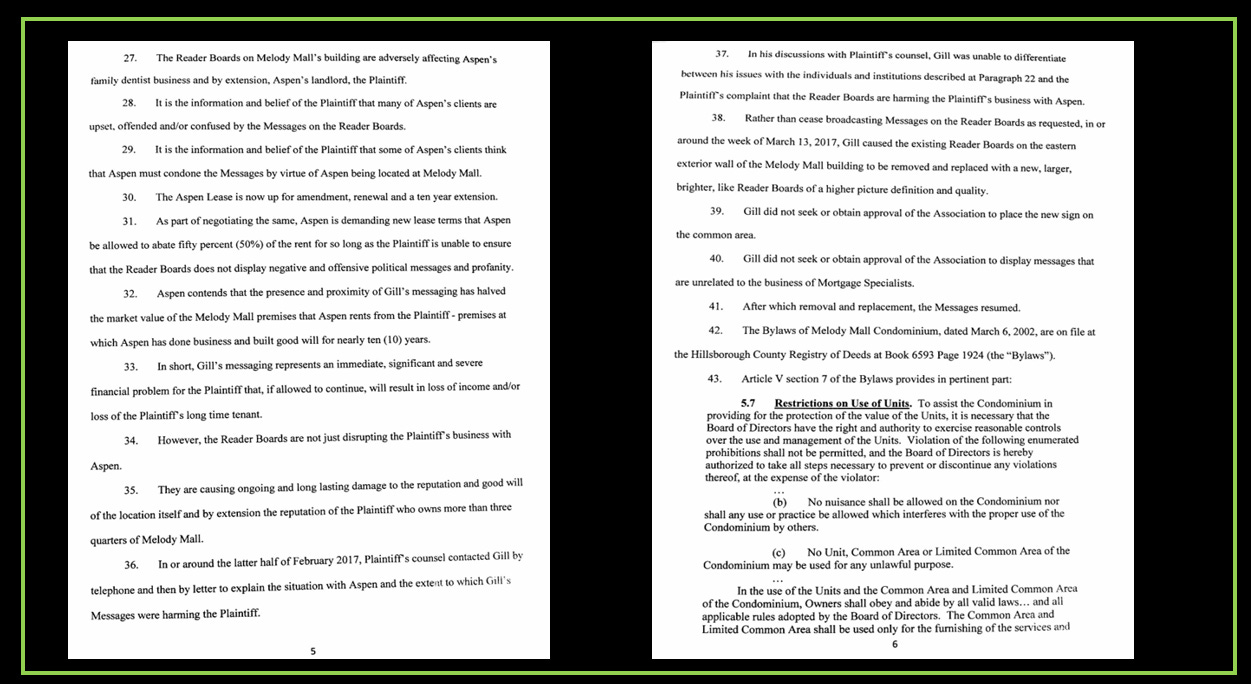

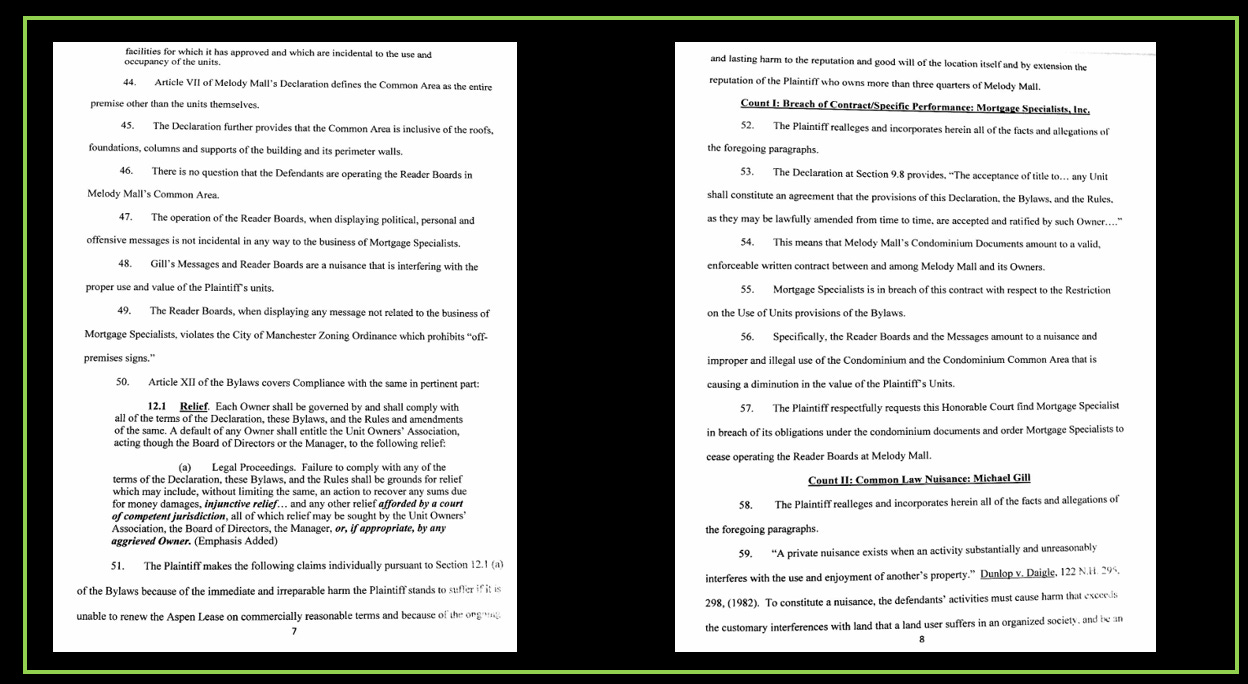

Here are some of the more frequent claims made on his broadcast and his website. Over the next two years he will rachet up his accusations. If you have been paying attention, thus far Mike’s only defense for his legal issues has been to blame others. His only evidence amounts to hearsay, as it is only “witnesses” who often need immunity. For someone who has already sued others twice over defamation, he sure waxes a salacious as he defames others. You can’t escape it either as he posts his defamatory statements on billboards, local am radio broadcasts, podcasts, social media and his website. All the while with NO real evidence.

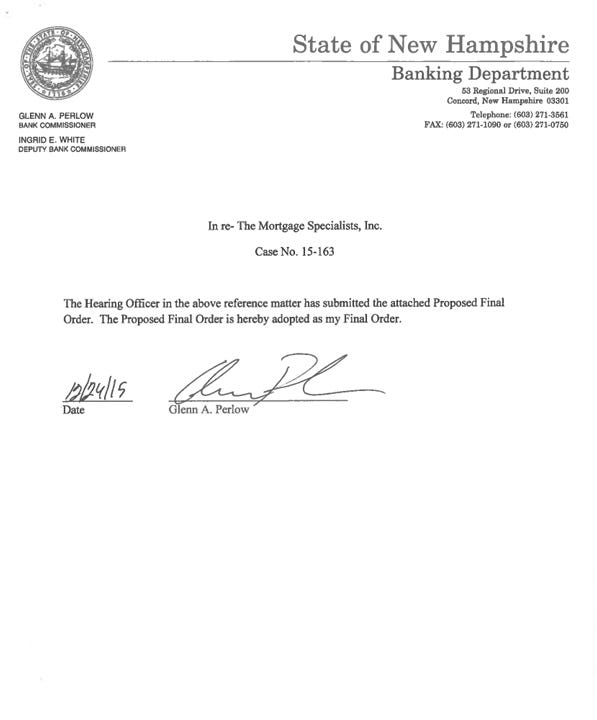

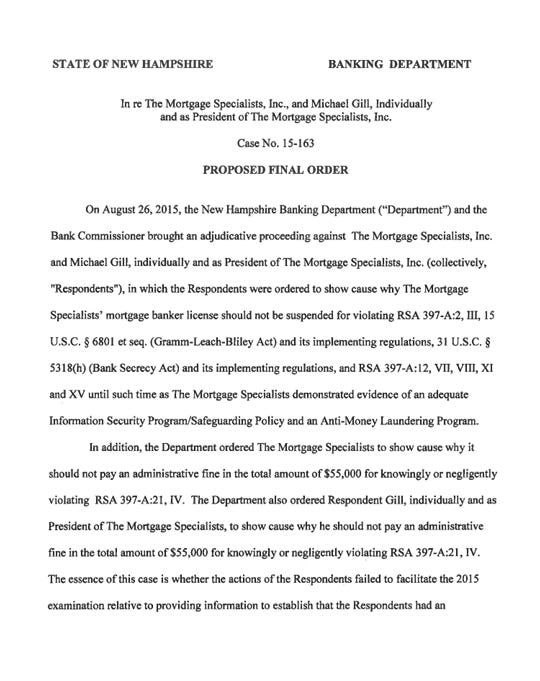

In April of 2013, The Mortgage Specialists were served an Order to Show Cause and Produce Records. They refused to comply. In September State Banking received a Default Judgement against the Morgage Specialists. In 14 years, Mortgage Specialists has been found with document issues, each time when inspected fraud is found. In August of 2015, MSI was served an Order to Show Cause, and in December of 2015 State Banking Issued their Final Order. Mike’s interruptions and outbursts on matters not related to the case at hand resulted in the court having to instruct the parties to submit a brief. On December 10, 2015, Mike severally and jointly as MSI was stripped of licensing.

The Emperor Has No Clothes

I am not going to belabor this because it is so characteristic of this individual. He wasn’t even registered to vote. No, I do not buy for a hot minute his conspiracy.

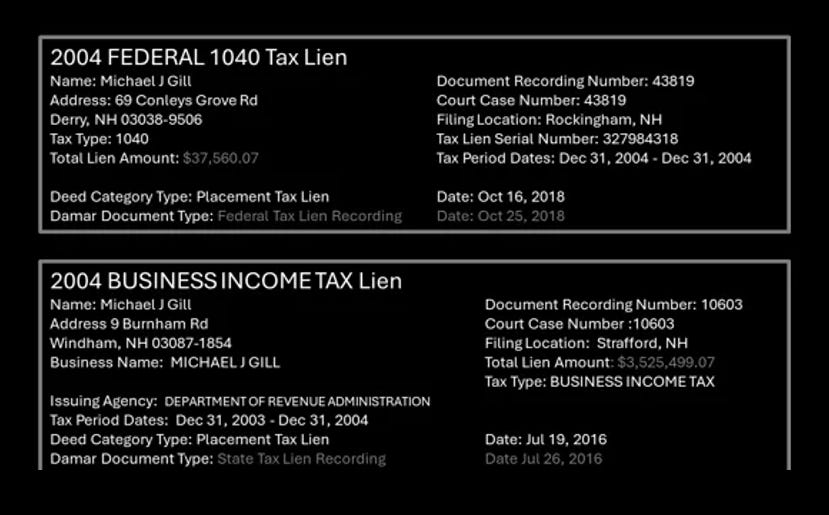

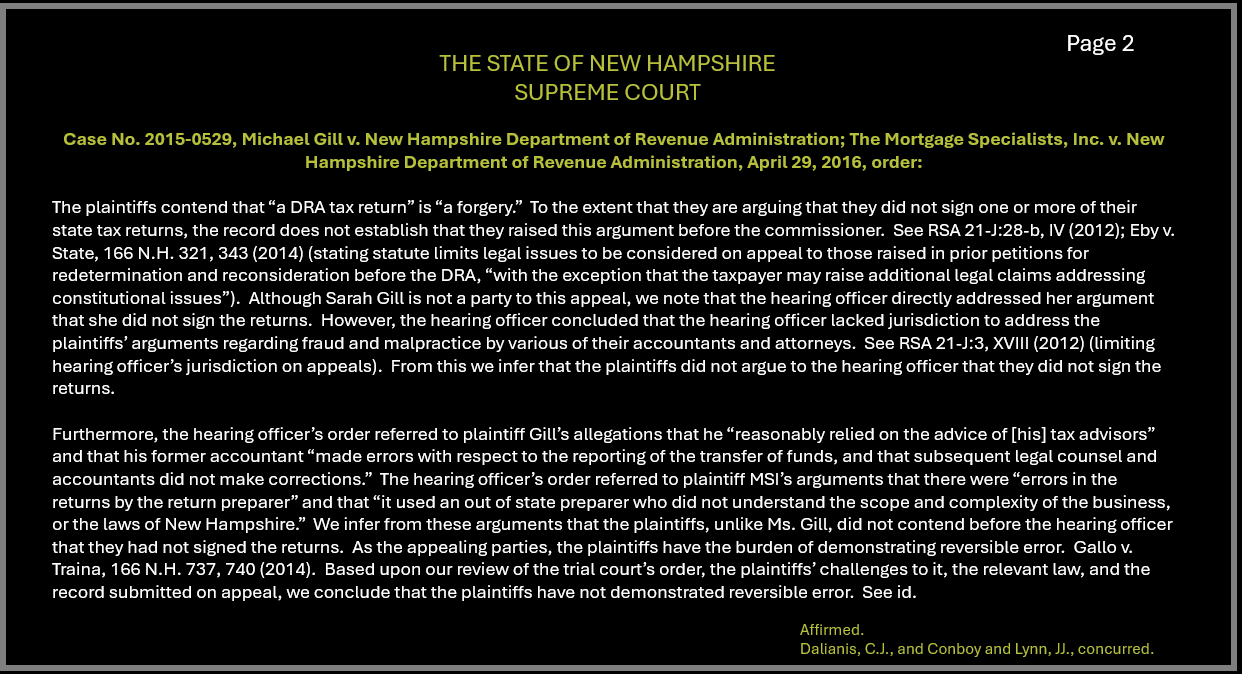

In 2016 The New Hampshire Department of Revenue brings suit as Mike’s taxes are not being resolved. His claim is his signature is a forgery, I did not sign those. Another conspiracy. Collectively across the various tax authorities he owes nearly 7.5 million in taxes.

Let’s hear Mike’s “recollection”.

“Mike and Sarah Gill ("Sarah") begin filing separate tax returns in 2008 for tax years beginning 2005. Prior to that, Sarah's friend Joseph Faletra ("Faletra") prepared and filed the personal and corporate tax returns with help from Sarah, in fact, Sarah worked with Faletra preparing the business expenses and the depreciation schedule for the horses for Mike Gill Racing.

In 2006, the IRS issued a notice of tax deficiency for 2001-2004. Mike and Sarah were represented by Williams and Connolly, CCR, LLP and Devine. Subsequently, during the divorce, Sarah was represented by Justin Holden. Sarah claimed innocent spouse in the IRS case and later in the divorce action.

The IRS issues began to arise when Walker referred Mike to CCR LLP as accountants.”

Grant Thornton later on purchased CCR LLP and CCR would have been obligated to disclose any wrong doings to Grant Thornton. Walker's cousin Bill Tarzia, was a partner with CCR. It was Lawrence Schwartz ("Larry") also a partner at CCR who took the lead on the tax work for Mike and MSI. Larry worked closely with Maurice Gilbert, Jon Sparkman and Walker both of Devine. Gilbert worked for the DRA as a Manager for 25 years. He was then hired by Devine and began working on Mike's case. Gilbert knows everyone in the DRA and Mike believes that he is the one who controlled the DRA piece inside the DRA for Walker. The trouble with the IRS began when information regarding Mike Gill Racing was intentionally incorrectly filed with the IRS. Several forms including a K-1 and Net Operating Loss (" OL") form were fraudulently prepared by the tax preparer (counseled by the attorneys) and filed by Michael Gill.

Gilbert was the one that spoke to the accountants to have the tax returns adjusted assuming Mike would take a settlement. But the settlement came with a leveraged $28 million on my K-1 form making it New Hampshire Income. Even though this was argued with the IRS calling the horse racing not a hobby but a business and Mike won Schwartz left the K-1 issue for Walker to fix. Once Schwartz was fired he sent the information to Marc Cohen ("Cohen") of Cohen+ Associates. Cohen called Mike and told him that Schwartz had dropped off the information. Cohen asked Schwartz directly about the NOL mistake and Schwartz had no response. Cohen also asked Schwartz about the issue with the K-1 when Schwartz and Walker were the one who argued the case for Mike and won. Schwartz then told Cohen that he had been instructed by Walker to put the information on the K-1 and that Walker would take care of the NH DRA. The information was put on the DRA to provide Walker with leverage against Mike and to legitimize the issues with the DRA release for Walker and was rejected by Mike.

Gilbert called the accounting firm of Berry Dunn. They refused to complete and file the taxes because the way Walker was requesting them to be completed was fraudulent. Schwartz ended up preparing them instead. BerryDunn called Lisa Tracy, the controller of MSI and indicated that Gilbert had previously told them that MSI had settled.

His responsibility was to screw up the NOL carry-back. It cost Mike close to $1 Million. It was a mistake that a junior accountant would not make. When the IRS began sending notices to correct the error, Larry did nothing. Schwartz also intentionally put thus putting leverage on Mike. Mike has now filed a criminal complaint with the IRS stating all of the facts. This was filed by Anthony Augeri. He intentionally screwed the complaint up. When it came to settling the IRS issues, Timothy Powell ("Powell") was the settlement agent on the case. When the settlement was presented to Mike, he was given less than a day to think about it and was told that Powell was retiring that next day. Three years later, with the IRS issues continuing, Mike found out that Powell had not retired and was in fact still the agent working on the issues surrounding Mike's tax returns.

Leverage on Mike…there’s just so much jockeying for leverage in his recollection. First of all, if it’s a mistake a junior accountant wouldn’t make, and you could see the problem why did you not resolve it? Second, leverage for what?? Who does this man envision himself to be? He is NOT that important except in his own mind. He is not intelligent either, he and wife discuss how they are going to file for 2005 in 2008 and your a rich successful businessman? Nope not buying it. In all of those words he uttered above he utter nothing except the most fantastical excuses I have ever heard.

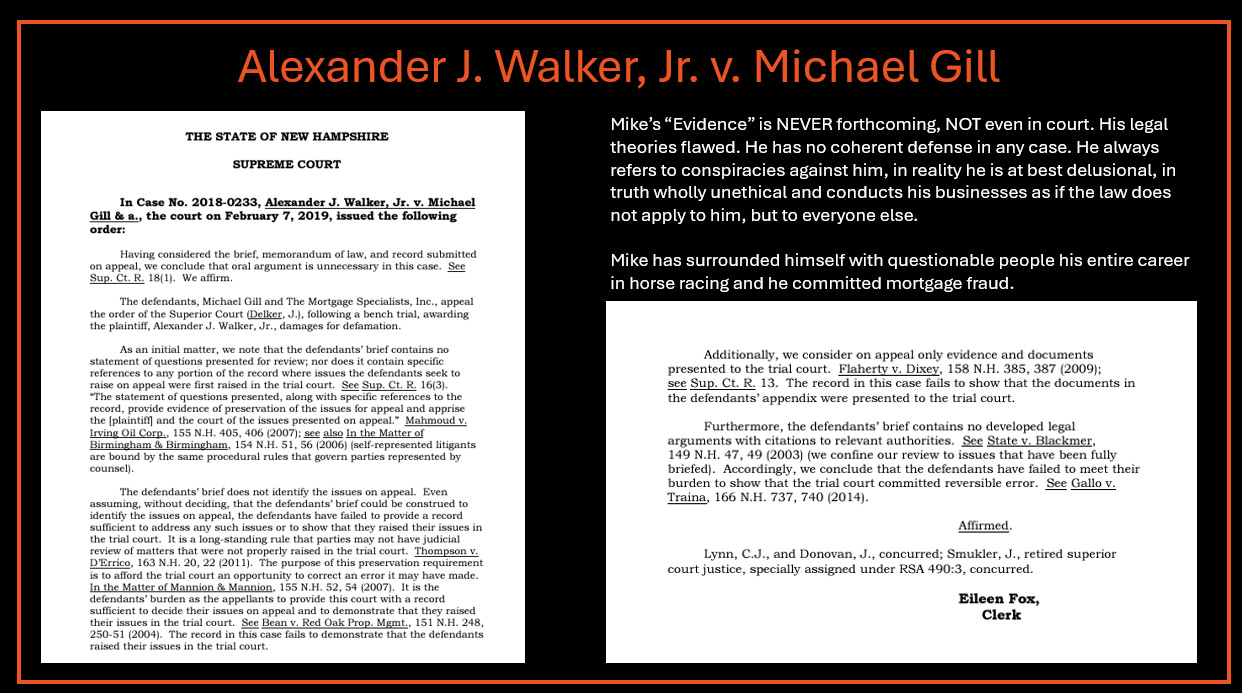

Well, it is 2016, seems Mike’s going to have his day in court and find out how a judge and jury feel about Mike’s his evidence. Surely, he is going to produce in court, right? I mean, how else can he defend against the defamation charges? He is going to have to submit real evidence of his claims. That evidence is going to be weighed by the jury.

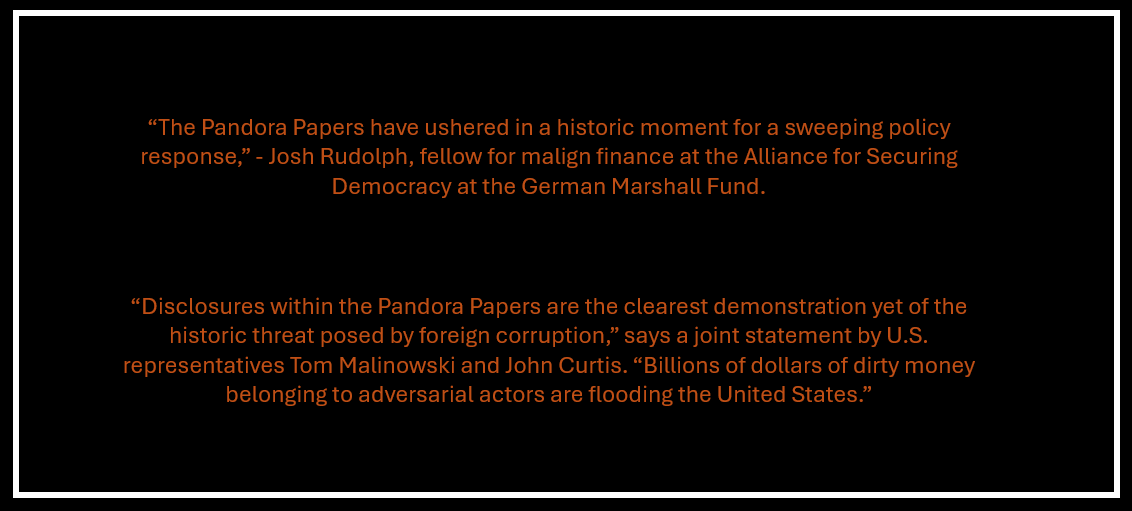

Circa 2021 Pandora Papers

The Pandora Papers are a release of nearly 12 million leaked documents that reveal the hidden and sometimes unethical or corrupt dealings of the global wealthy and elite—including prominent world leaders, politicians, corporate executives, celebrities, and billionaires. It was the largest investigation in journalism history.

2022

Circa 2023

Arizona Adventures - 2024

Mike comes out and Matthew serves as his guide for the AZ GOP. Thats what we were told any way.

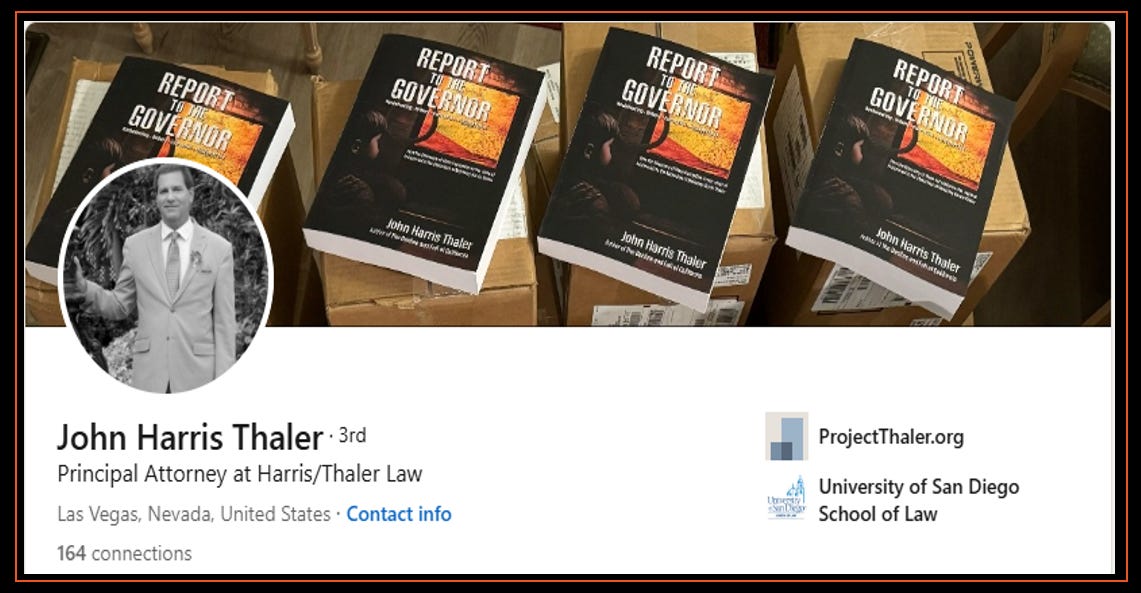

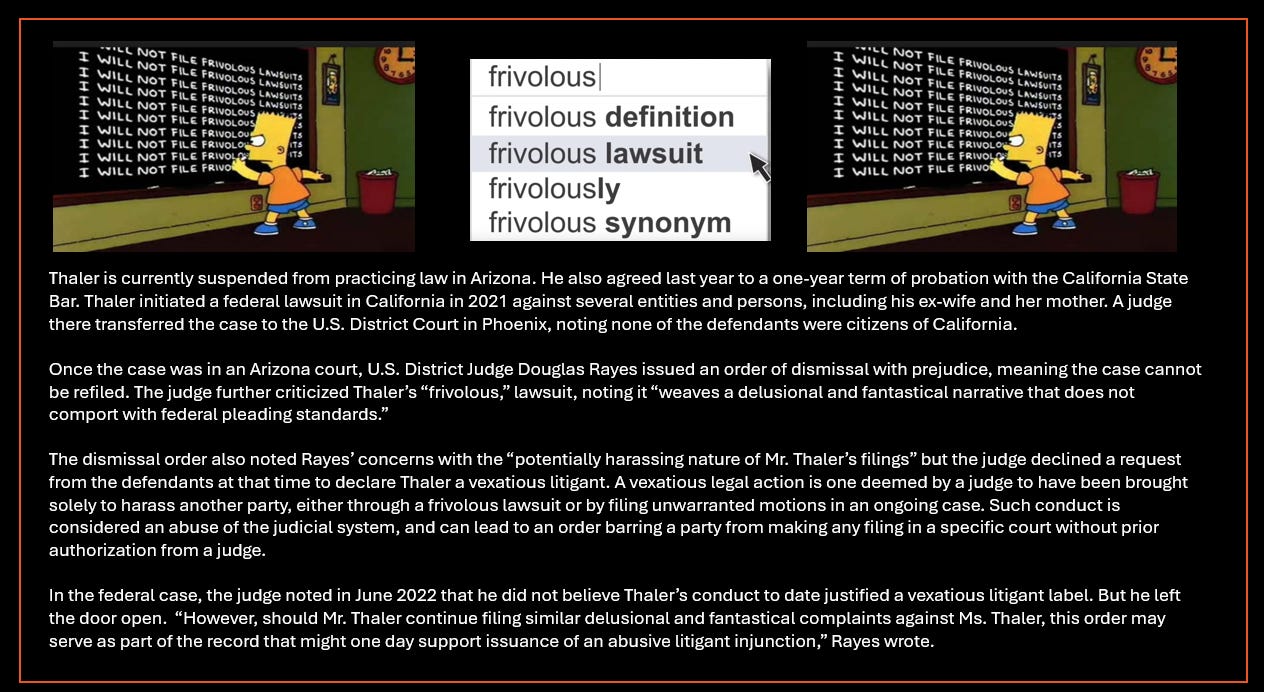

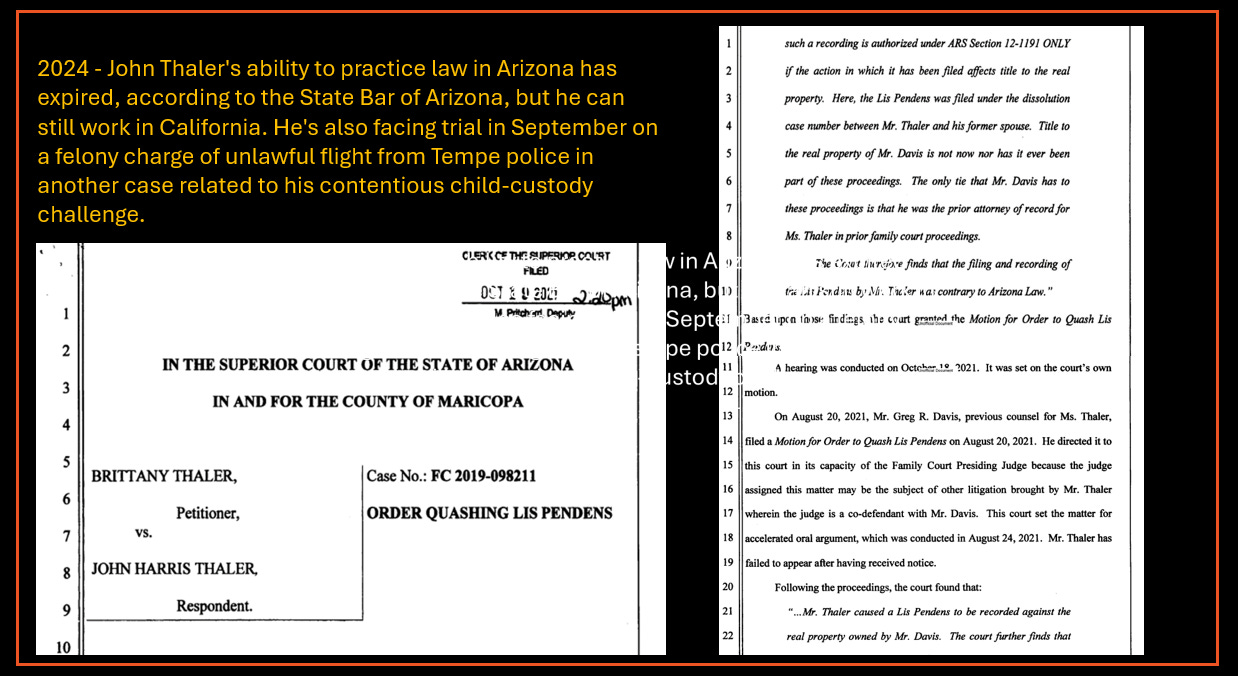

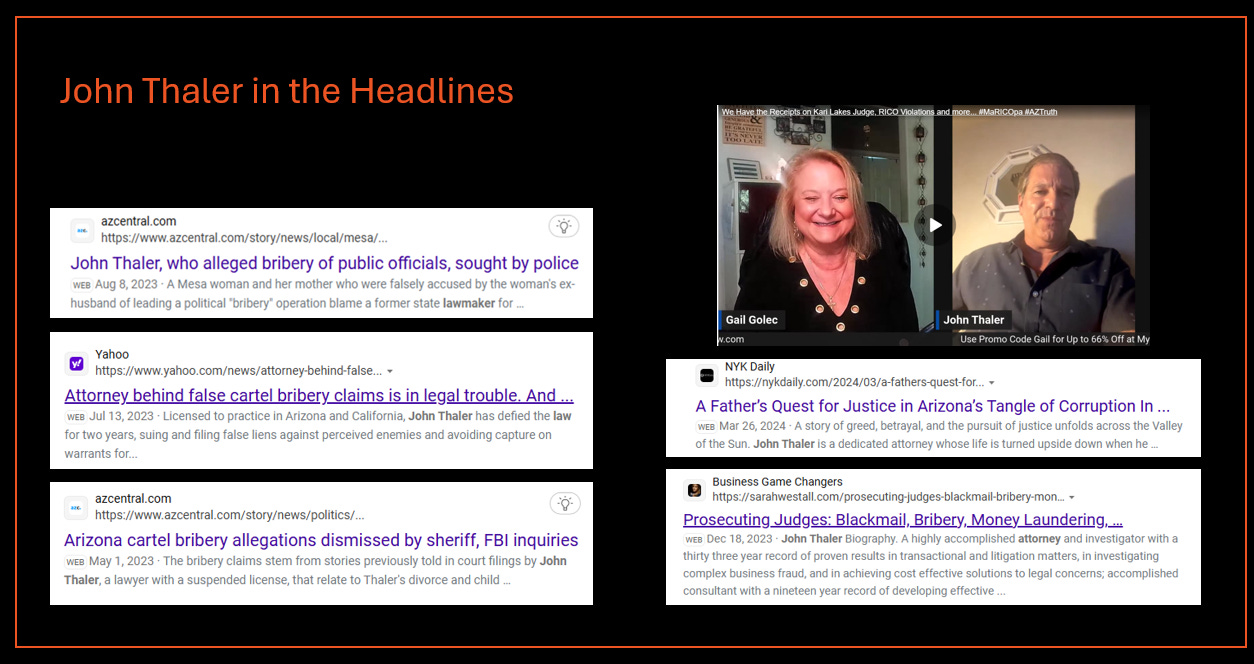

He also met with this attorney. Attorney Thaler and Mike share the same narrative villains, ex-wife, the cartel, Cartel Katie and you guessed it, no evidence.

You really just can’t make this up.

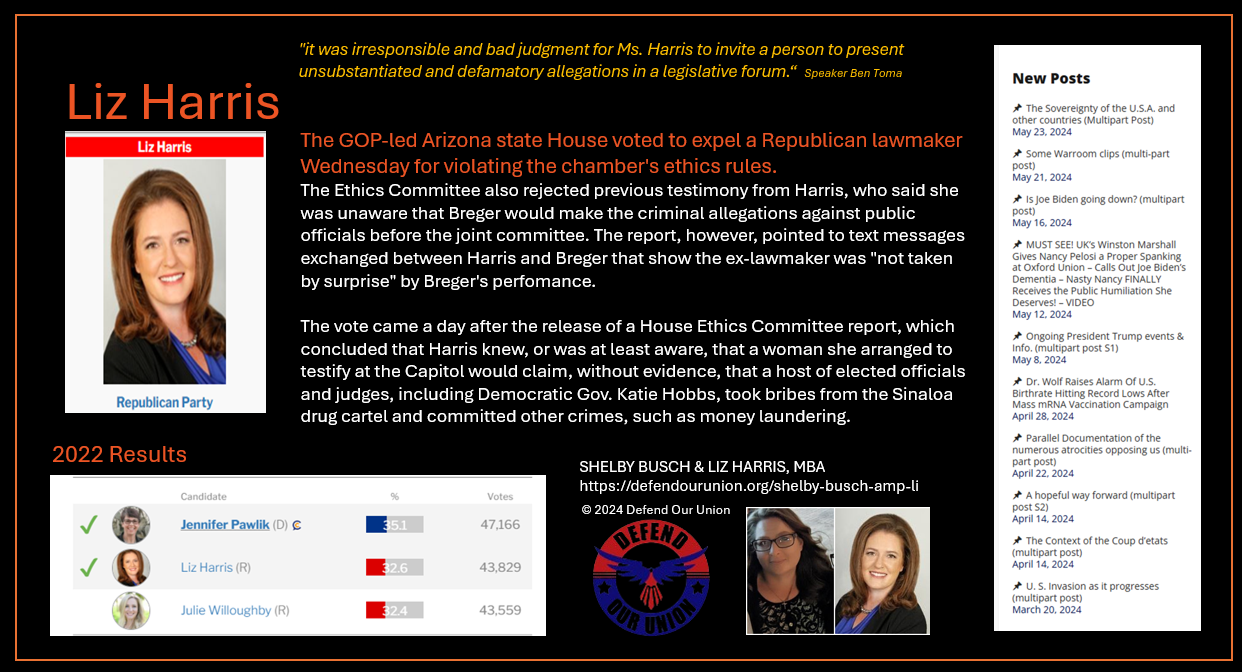

And we can’t forget Liz Harris, who was expelled for introducing Thaler’s girlfriend who levied the salacious allegations of Attorney Thaler in session with NO evidence whatsoever.

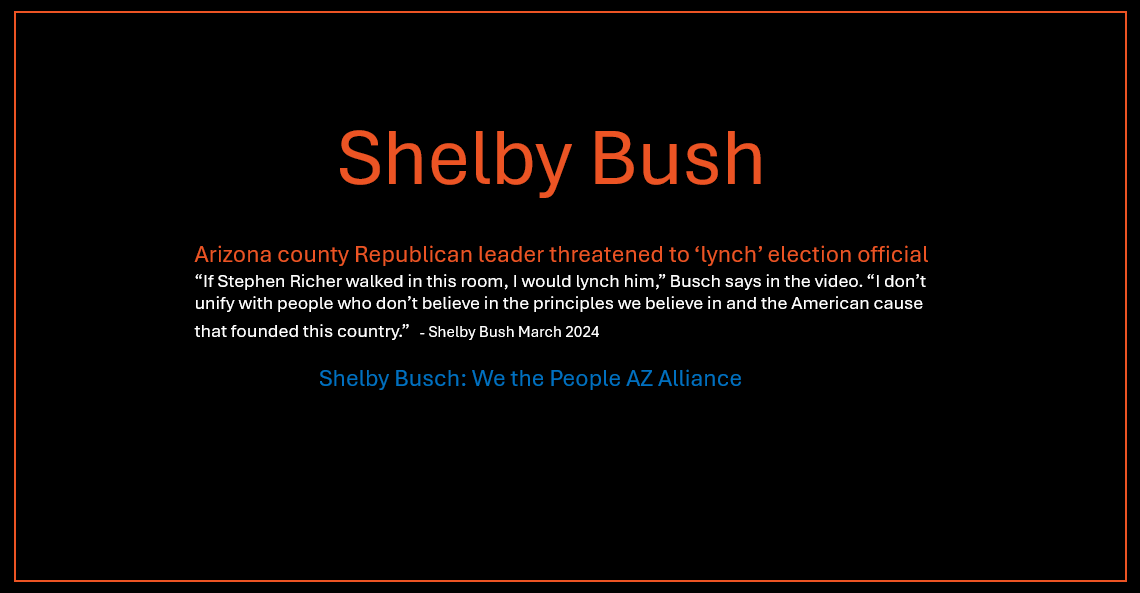

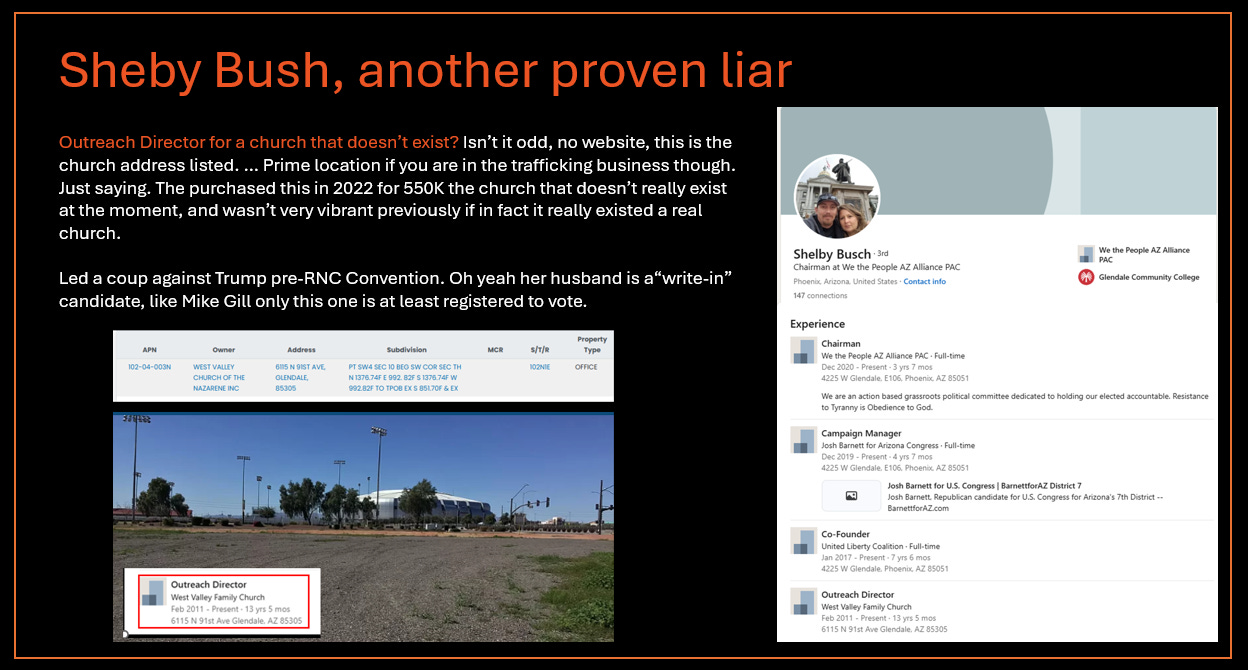

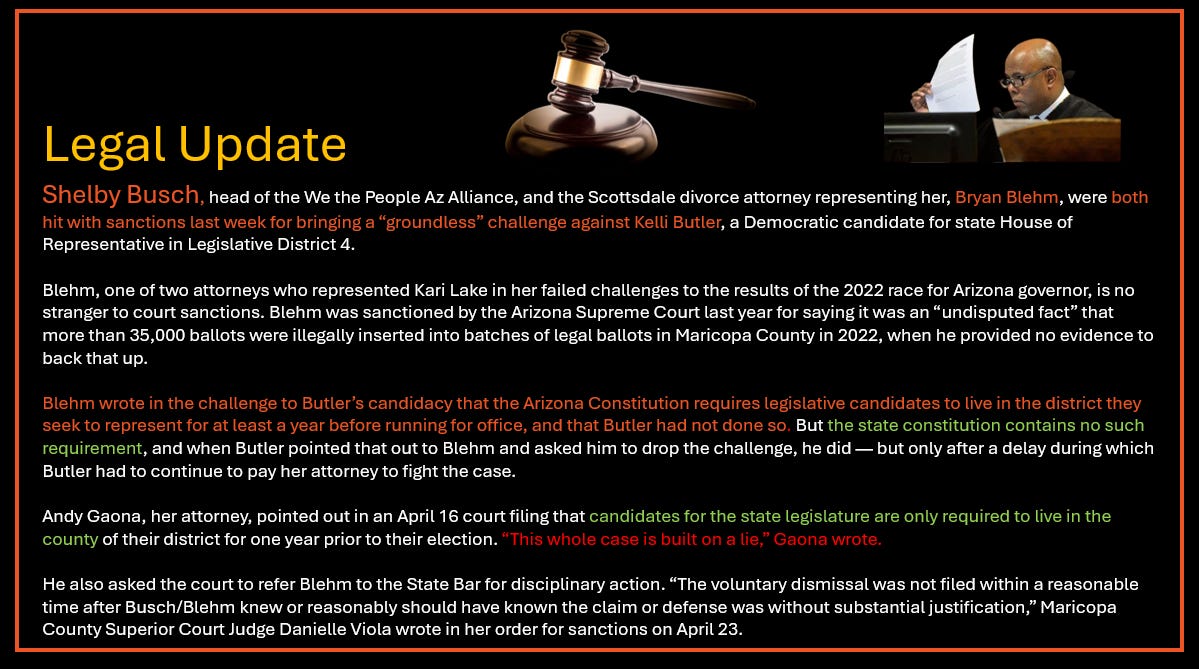

And then Shelby Bush, who tried to lead a coup of the electors against Trump at the Convention. Mike tries to claim after carousing with the most controversial folks, that he came to save Trump. Please.

Mike’s current grift, give today and tomorrow he will surely slander you.